A firm wishing to evaluate interest rate behavior has gathered data on the nominal rate of interest

Question:

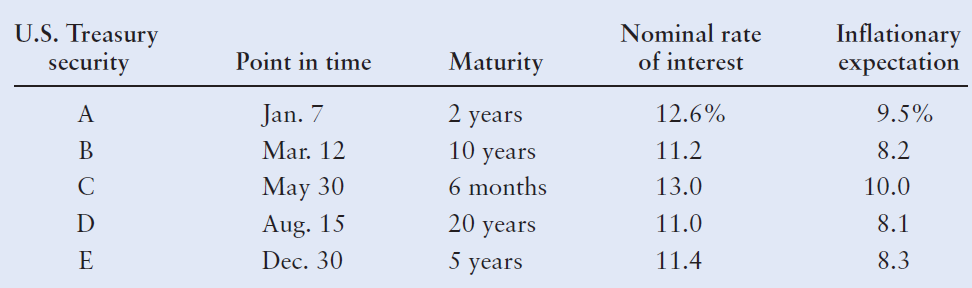

A firm wishing to evaluate interest rate behavior has gathered data on the nominal rate of interest and on inflationary expectations for five U.S. Treasury securities, each having a different maturity and each measured at a different point in time during the year just ended. (Note: Assume that the risk that future interest rate movements will affect longer maturities more than shorter maturities is zero; that is, there is no maturity risk.) These data are summarized in the following table.

a. Using the preceding data, find the real rate of interest at each point in time.

b. Describe the behavior of the real rate of interest over the year. What forces might be responsible for such behavior?

c. Draw the yield curve associated with these data, assuming that the nominal rates were measured at the same point in time.

d. Describe the resulting yield curve in part c, and explain the general expectations embodied init.

"Nominal interest rate refers to the interest rate before taking inflation into account. Nominal can also refer to the advertised or stated interest rate on a loan, without taking into account any fees or compounding of interest. The nominal...

Step by Step Answer:

Real rate of interest r r i r IP RP RP 0 for Treasury issues r r i IP a Security Nominal Rate r j ...View the full answer

Principles Of Managerial Finance

ISBN: 978-0136119463

13th Edition

Authors: Lawrence J. Gitman, Chad J. Zutter