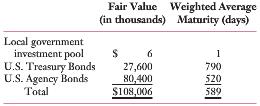

A note from the annual report of a city includes the following: As of September 30, the

Question:

A note from the annual report of a city includes the following: As of September 30, the utility fund had the following investments:

Credit risk. As of September 30, the U.S. Treasuries and the U.S. Agency Bonds were rated AAA by Standard & Poor’s. The local government investment pool was rated AA.

Interest rate risk. As a means of minimizing risk of loss due to interest rate fluctuations, the investment policy requires that the dollar-weighted average maturity using final stated maturity dates shall not exceed seven years. The portfolio’s weighted average maturity, however, may be substantially shorter if market conditions so dictate. As of September 30, the dollar-weighted average maturity was 589 days (1.61 years).

1. Why would the city limit the weighted average maturity of its portfolio to seven years rather than a greater number of years, even though investments with a longer maturity generally provide a greater investment yield?

2. Why might the city indicate that the average maturity of the local government investment pool is only one day when, in fact, the pool holds investments that have an average maturity of over thirty days?

3. What is meant by ‘‘credit risk?’’ How would you assess the credit risk of the U.S. Treasury and U.S. agency bonds? Explain.

PortfolioA portfolio is a grouping of financial assets such as stocks, bonds, commodities, currencies and cash equivalents, as well as their fund counterparts, including mutual, exchange-traded and closed funds. A portfolio can also consist of non-publicly...

Step by Step Answer:

1 The city limits the maturity dates of its investments because the long...View the full answer

Government and Not for Profit Accounting Concepts and Practices

ISBN: 978-1118155974

6th edition

Authors: Michael H. Granof, Saleha B. Khumawala