Auditors typically will find the items lettered AF in a client-prepared bank reconciliation. Required : Assume these

Question:

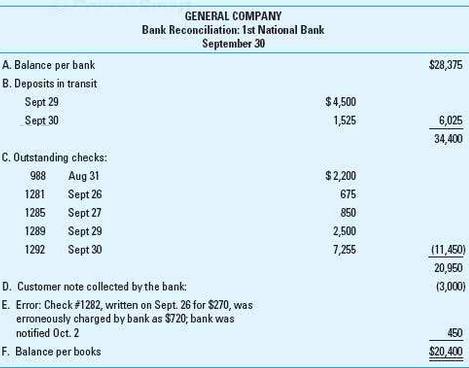

Auditors typically will find the items lettered A–F in a client-prepared bank reconciliation.

Required:

Assume these facts: On October 11, the auditor received a cutoff bank statement dated October 7. The September 30 deposit in transit; the outstanding checks 1281, 1285, 1289, and 1292; and the correction of the bank error regarding check 1282 appeared on the cutoff bank statement.

a. For each of the preceding lettered items A– F, select one or more of the following procedures 1– 10 that you believe the auditor should perform to obtain evidence about the item. These procedures may be selected once, more than once, or not at all. Be prepared to explain the reasons for your choices.

1. Trace to cash receipts journal.

2. Trace to cash disbursements journal.

3. Compare to the September 30 general ledger.

4. Confirm directly with the bank.

5. Inspect bank credit memo.

6. Inspect bank debit memo.

7. Ascertain reason for unusual delay, if any.

8. Inspect supporting documents for reconciling items that do not appear on the cutoff bank statement.

9. Trace items on the bank reconciliation to the cutoff bank statement.

10. Trace items on the cutoff bank statement to the bank reconciliation.

b. Auditors ordinarily foot a client- prepared bank reconciliation. If the auditors had per-formed this recalculation on the preceding bank reconciliation, what might they have found? Be prepared to discuss any findings.

Step by Step Answer:

a Identification of procedures A Balance per bank pr...View the full answer

Auditing and Assurance Services

ISBN: 978-0077862343

6th edition

Authors: Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws