Ball OFluff Company manufactures and ships childrens stuffed animals across the nation. The following are profit statements

Question:

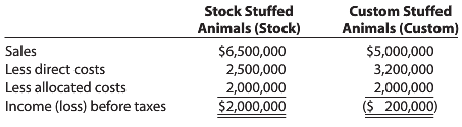

Ball O’Fluff Company manufactures and ships children’s stuffed animals across the nation. The following are profit statements for the company’s two lines of business:

Costs that are easily associated with each line of business are included in the direct costs. Allocated costs include costs that are not directly traced to the business units. These costs include employee benefits, rent, telecommunications costs, and general and administrative costs, such as the salary of the CEO of Ball 0’ Fluff.

At the start of 2011, allocated costs were estimated as follows:

Employee benefits$1...........$1,000,000

Rent................. 1,500,000

Telecommunications............ 500,000

General and administrative costs..... 1,000,000

Total.................$4,000,000

In the past, allocations have been based on headcount (the number of employees in each business unit).There were 240 employees in Stock and 80 employees in Custom. The new controller of Ball 0’ Fluff believes that the key driver of employee benefits and telecommunications costs is headcount. However, rent is driven by space occupied, and general and administrative cost are driven by relative sales. Ball 0’ Fluff rents 20,000 square feet; approximately 10,000 is occupied by Stock employees and 10,000 by Custom personnel.

Required

a. Prepare profit reports for Stock and Custom, assuming the company allocates costs using headcount, space occupied, and sales as allocation bases. Compare the new levels of profit to the levels that result using a single allocation base (headcount).Round to two decimal places.

b. Which provides the best information on profitability: a single overhead cost pool with head- count as the allocation base, or multiple cost pools using headcount, sales, and space occupied?

Step by Step Answer:

a Allocation Base Stock Stuffed Animals Custom Stuffed Animals Employee Benefits Head count 240 80 P...View the full answer