FIFO and LIFO Effects You are the vice president of finance of Mickiewicz Corporation, a retail company

Question:

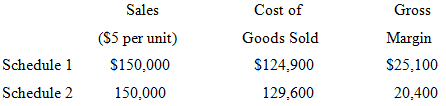

FIFO and LIFO Effects You are the vice president of finance of Mickiewicz Corporation, a retail company that prepared two different schedules of gross margin for the first quarter ended March 31, 2010. These schedules appear below.

The computation of cost of goods sold in each schedule is based on the following data. Peggy Fleming, the president of the corporation, cannot understand how two different gross margins can be computed from the same set of data. As the vice president of finance you have explained to Ms. Fleming that the two schedules are based on different assumptions concerning the flow of inventory costs, i.e., FIFO and LIFO. Schedules 1 and 2 were not necessarily prepared in this sequence of cost flow assumptions. Prepare two separate schedules computing cost of goods sold and supporting schedules showing the composition of the ending inventory under both cost flow assumptions (assume periodic system).

.PNG)

The ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =...

Step by Step Answer:

MICKIEWICZ CORPORATION Schedules of Cost of Goods Sold For the First Quarter End...View the full answer

Intermediate Accounting

ISBN: 978-0470423684

13th Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield