Case A. Dr Pepper Snapple Group, Inc., is a leading integrated brand owner, bottler, and distributor of

Question:

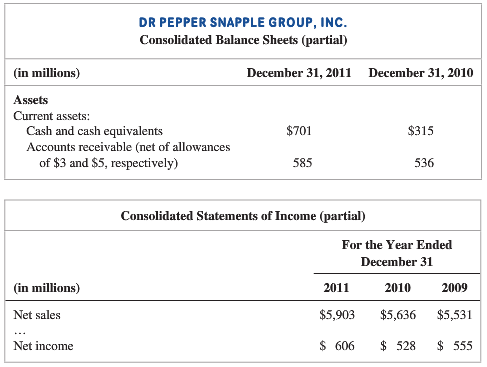

Case A. Dr Pepper Snapple Group, Inc., is a leading integrated brand owner, bottler, and distributor of nonalcoholic beverages in the United States, Canada, and Mexico. Key brands include Dr. Pepper, Snapple, 7-UP, Mott’s juices, A&W root beer, Canada Dry ginger ale, Schweppes ginger ale, and Hawaiian Punch, among others.

The following represents selected data from recent financial statements of Dr Pepper Snapple Group (dollars in millions):

The company also reported bad debt expense of $4 million in 2011, $1 million in 2010, and $3 million in 2009.

1. Record the company’s write-offs of uncollectible accounts for 2011.

2. Assuming all sales were on credit, what amount of cash did Dr Pepper Snapple Group collect from customers in 2011?

3. Compute the company’s net profit margin for the three years presented. What does the trend suggest to you about Dr Pepper Snapple Group?

Case B. Samuda Enterprises uses the aging approach to estimate bad debt expense. At the end of 2014, Samuda reported a balance in accounts receivable of $620,000 and estimated that $12,400 of its accounts receivable would likely be uncollectible. The allowance for doubtful accounts has a $1,500 debit balance at year-end (that is, more was written off during the year than the balance in the account).

1. What amount of bad debt expense should be recorded for 2014?

2. What amount will be reported on the 2014 balance sheet for accounts receivable?

Case C. At the end of 2015, the unadjusted trial balance of Samuels, Inc., indicated $6,530,000 in Accounts Receivable, a credit balance of $9,200 in Allowance for Doubtful Accounts, and Sales Revenue (all on credit) of $155,380,000. Based on knowledge that the current economy is in distress, Samuels increased its bad debt rate estimate to 0.3 percent on credit sales.

1. What amount of bad debt expense should be recorded for 2015?

2. What amount will be reported on the 2015 balance sheet for accounts receivable?

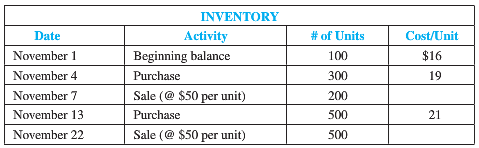

Case D. Stewart Company reports the following inventory records for November 2014:

Selling, administrative, and depreciation expenses for the month were $16,000. Stewart’s tax rate is 30 percent.

1. Calculate the cost of ending inventory and the cost of goods sold under each of the following methods:

a. First-in, first-out.

b. Last-in, first out.

c. Weighted average (round unit cost to the nearest penny.)

2. Based on your answers in requirement (1)

a. What is the gross profit percentage under the FIFO method?

b. What is net income under the LIFO method?

c. Which method would you recommend to Stewart for tax and financial reporting purposes?

Explain your recommendation.

3. Stewart applied the lower of cost or market method to value its inventory for reporting purposes at the end of the month. Assuming Stewart used the FIFO method and that inventory had a market replacement value of $19.50 per unit, what would Stewart report on the balance sheet for inventory? Why?

Case E. Matson Company purchased the following on January 1, 2014:

• Office equipment at a cost of $60,000 with an estimated useful life to the company of three years and a residual value of $15,000. The company uses the double-declining-balance method of depreciation for the equipment.

• Factory equipment at an invoice price of $880,000 plus shipping costs of $20,000. The equipment has an estimated useful life of 100,000 hours and no residual value. The company uses the units-of-production method of depreciation for the equipment.

• A patent at a cost of $330,000 with an estimated useful life of 15 years. The company uses the straight-line method of amortization for intangible assets with no residual value.

1. Prepare a partial depreciation schedule for 2014, 2015, and 2016 for the following assets (round your answers to the nearest dollar):

a. Office equipment.

b. Factory equipment. The company used the equipment for 8,000 hours in 2014, 9,200 hours in 2015, and 8,900 hours in 2016.

2. On January 1, 2017, Matson altered its corporate strategy dramatically. The company sold the factory equipment for $700,000 in cash. Record the entry related to the sale of the factory equipment.

3. On January 1, 2017, when the company changed its corporate strategy, its patent had estimated future cash flows of $210,000 and a fair value of $190,000. What would the company report on the income statement (account and amount) regarding the patent on January 2, 2017? Explain your answer.

An intangible asset is a resource controlled by an entity without physical substance. Unlike other assets, an intangible asset has no physical existence and you cannot touch it.Types of Intangible Assets and ExamplesSome examples are patented... Ending Inventory

The ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =... Financial Statements

Financial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial... Accounts Receivable

Accounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that... Balance Sheet

Balance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial...

Step by Step Answer:

Case A Req 1 in millions Allowance for uncollectible accounts XA A 1 6 Accounts receivable A 6 Req 2 Cash collections for 2008 2 were 5850 million 1 Beg allowance 5 Bad debt expense 4 Writeoffs End Al...View the full answer

Financial Accounting

ISBN: 978-0078025556

8th edition

Authors: Robert Libby, Patricia Libby, Daniel Short