Christine Morrison, treasurer of Salt Lake Light Opera (SLLO), was preparing a loan request to the South

Question:

Christine Morrison, treasurer of Salt Lake Light Opera (SLLO), was preparing a loan request to the South Utah National Bank in December 20X4. The loan was necessary to meet the cash needs of the SLLO for year 20X5. In a few short years, the SLLO had established itself as a premier opera company. In addition to its regular subscription series, it started a series for new composers and offered a very popular holiday production. The holiday production was the most financially successful of the SLLO’s activities, providing a base to support innovative productions that were artistically important to the SLLO but did not usually succeed financially.

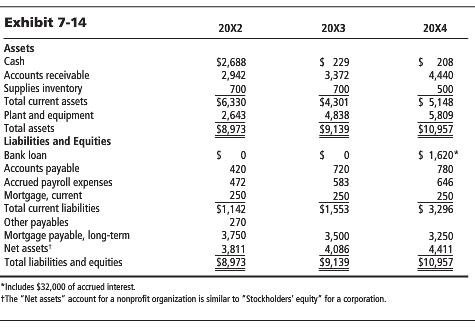

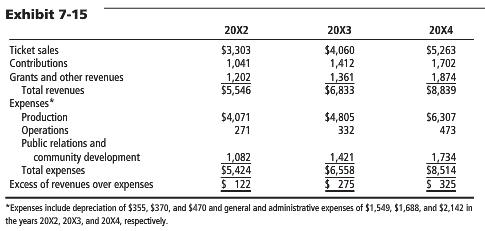

In total, the SLLO had done well financially, as shown in Exhibits 7-14 and 7-15. Its profitable operations had enabled it to build its own building and generally acquire a large number of assets. It had at least broken even every year since its incorporation, and management anticipates continued profitable operations. The Corporate Community for the Arts in Salt Lake and several private foundations had made many grants to the SLLO, and such grants are expected to continue. Most recently, the largest bank in town had agreed to sponsor the production of a new opera by a local composer. The SLLO’s director of development, Harlan Wayne, expected such corporate sponsorships to increase in the future.

To provide facilities for the Opera’s anticipated growth, SLLO began work on an addition to its building 2 years ago. The new facilities are intended primarily to support the experimental offerings that were becoming more numerous. The capital expansion was to be completed in 20X5; all that remained was acquisition and installation of lighting, sound equipment, and other new equipment to be purchased in 20X5.

SLLO had borrowed working capital from South Utah National Bank for the past several years.

To qualify for the loans, the SLLO had to agree to the following:

1. Completely pay off the loan for 1 month during the course of the year.

2. Maintain cash and accounts receivable balances equal to (or greater than) 120% of the loan.

3. Maintain a compensating cash balance of $200,000 at all times.

In the past, the SLLO has had no problem meeting these requirements. However, in 20X4 the

SLLO had been unable to reduce the loan to zero for an entire month. Although South Utah continued to extend the needed credit, the loan manager expressed concern over the situation. She asked for a quarterly cash budget to justify the financing needed for 20X5. Ms. Morrison began to assemble the data needed to prepare such a budget.

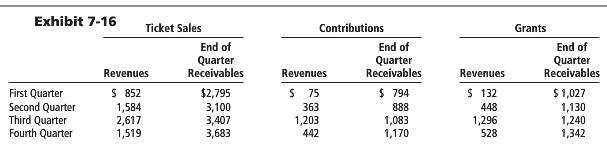

SLLO received revenue from three main sources: ticket sales, contributions, and grants.

Ms. Morrison formed Exhibit 7-16 to calculate the accounts receivable balance for each of these sources for 20X5. She assumed that SLLO would continue its normal practices for collecting pledges and grant revenues.

Most expenses were constant from month to month. An exception was supplies, which were purchased twice a year in December and June. In 20X5, SLLO expects to purchase $200,000 of supplies in June and $700,000 in December on terms of net, 30 days. The supplies inventory at the end of December was expected to be $600,000. Depreciation expense of $500,000 was planned for 20X5, and other expenses were expected to run at a steady rate of $710,000 a month throughout the year, of which $700,000 was payroll costs. Salaries and wages were paid on the Monday of the first week following the end of the month. The remaining $10,000 of other expenses were paid as incurred.

The major portion of the new equipment to be installed in 20X5 was to be delivered in September; payments totaling $400,000 would be made in four equal monthly installments beginning in September.

In addition, small equipment purchases are expected to run $20,000 per month throughout the year. They will be paid for on delivery.

In late 20X2, SLLO had borrowed $4 million (classified as a mortgage payable) from Farmers’ Life Insurance Company. The SLLO is repaying the loan over 16 years, in equal principal payments in June and December of each year. Interest at 8% annually is also paid on the unpaid balance on each of these dates. Total interest payments for 20X5, according to Ms. Morrison’s calculations, would be $275,000.

Interest on the working capital loan from South Utah National Bank was at an annual rate of 10%.

Interest is accrued quarterly but paid annually; payment for 20X4’s interest would be made on January 10, 20X5, and that for 20X5’s interest would be made on January 10, 20X6. Working capital loans are taken out on the first day of the quarter that funds are needed, and they are repaid on the last day of the quarter when extra funds are generated. SLLO has tried to keep a minimum cash balance of $200,000 at all times, even if loan requirements do not require it.

1. Compute the cash inflows and outflows for each quarter of 20X5. What are SLLO’s loan requirements each quarter?

2. Prepare a projected income statement and balance sheet for SLLO for 20X5.

3. What financing strategy would you recommend for SLLO?

Balance SheetBalance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial... Cash Budget

A cash budget is an estimation of the cash flows for a business over a specific period of time. These cash inflows and outflows include revenues collected, expenses paid, and loans receipts and payment. Its primary purpose is to provide the...

Step by Step Answer:

1 On January 1 Salt Lake Light Opera needs to borrow 2057000 on April 1 it needs an additional 562000 on September 31 it can repay 2014000 but on Octo...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta