Cleveland Plastics makes plastic parts for other manufacturing companies. Cleveland has an ABC system for its production,

Question:

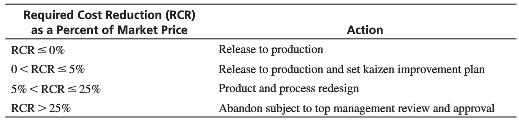

Cleveland Plastics makes plastic parts for other manufacturing companies. Cleveland has an ABC system for its production, marketing, and customer service functions. The company uses target costing as a strategic decision-making tool. One of Cleveland’s product lines—consumer products—has over 100 individual products with life cycles of less than 3 years. This means that about 30–40 products are discontinued and replaced with new products each year. Cleveland’s top management has established the following tool to be used by the target-cost team for evaluating proposed new products:

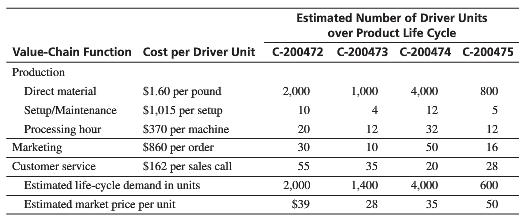

The following operational and ABC data are for four proposed new products:

Top management has set a desired contribution to cover unallocated value-chain costs, taxes, and profit of 40% of the estimated market price.

Prepare a schedule that shows for each proposed new product, the target cost, estimated cost using existing technology, and any required cost reduction as a percent of the estimated market price. Use the evaluation tool to make a decision regarding the four proposed new products.

Step by Step Answer:

Cost per driver unit C200472 C200473 C200474 C200475 Number of units Cost Number of units Cost ...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta