DVDS manufactures and sells DVD players in two countries. It manufactures two models Basic and Custom in

Question:

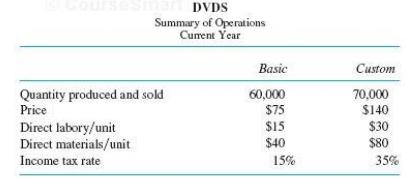

DVDS manufactures and sells DVD players in two countries. It manufactures two models— Basic and Custom— in the same plant. The Basic DVD has fewer options and provides lower- quality out-put than the Custom DVD. The basic model is sold only in a developing country and the custom model is sold only in a developed country. DVDS pays income taxes to the country where the final sale of the DVD player takes place. The following table summarizes DVDS operations.

Besides direct materials and direct labor, manufacturing overhead amounts to $ 2 million and is currently assigned to products based on direct labor dollars. Manufacturing overhead is a fixed cost ( does not vary with the number of units produced).

Required:

a. Calculate the unit manufacturing costs of the Basic and Custom DVD models using traditional absorption costing. Manufacturing overhead is allocated based on direct labor dollars.

b. DVDS hires a consulting firm to analyze its costing methods. After performing an extensive review, the consultants determine that the vast majority of the $ 2 million of o verhead varies with the number of different parts in the two DVD models. The number of parts drives purchasing department activities. More engineering time is spent on the more complex Custom DVD models. More accounting depreciation of assembly and testing equipment is incurred producing the Custom DVD model than the Basic DVD model. The Basic DVD has 140 different parts and the Custom DVD model has 160 different parts. Calculate the unit manufacturing costs of the Basic and Custom DVD models using activity- based costing.

c. Should DVDS change its costing methodology from its traditional absorption costing to ABC? Explain why it should or should not.

Step by Step Answer:

a Unit manufacturing costs of Basic and Custom DVDs using traditional absorption costing Manufacturing overhead is allocated based on direct labor dollars Basic Custom Total Quantity 60000 70000 Direc...View the full answer

Accounting for Decision Making and Control

ISBN: 978-0078025747

8th edition

Authors: Jerold Zimmerman