Examine Nikes segments as defined in Note 18 to its financial statements in the 10-K report in

Question:

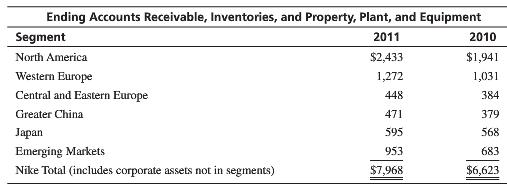

Examine Nike’s segments as defined in Note 18 to its financial statements in the 10-K report in Appendix C. We will use the segment information from the first six segments listed to calculate approximations to ROI and economic profit. For purposes of this problem, define segment income as segment EBIT and define segment assets as the sum of the assets shown in note 18, namely receivables, inventory, and property plant and equipment. Therefore, pretax and pre-interest ROA is EBIT divided by segment assets and an approximation to economic profit is EBIT minus a charge for the cost of capital to finance segment assets.

Using these definitions, determine ROA and economic profit for each segment in 2010 and 2011 using EBIT from Note 18 in the 10-K and the information on segment assets in the following table. Assume that Nike’s cost of capital is 10%. Use your results to evaluate the performance of each segment. Which segment management seems to be doing the best job? What subjective factors would you consider, in addition to ROA and economic profit, in assessing segment performance?

Financial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial... Cost Of Capital

Cost of capital refers to the opportunity cost of making a specific investment . Cost of capital (COC) is the rate of return that a firm must earn on its project investments to maintain its market value and attract funds. COC is the required rate of...

Step by Step Answer:

All amounts in this solution except percentages are in millions of dollars The North America segment produced the most economic profit both years and ...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta