Flexible-budget and sales volume variances. Marron, Inc. produces the basic fillings used in many popular frozen desserts

Question:

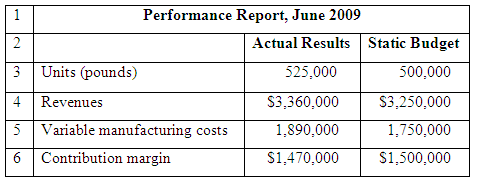

Flexible-budget and sales volume variances. Marron, Inc. produces the basic fillings used in many popular frozen desserts and treats—vanilla and chocolate ice creams, puddings, meringues, and fudge. Marron uses standard costing and carries over no inventory from one month to the next. The ice-cream product group’s results for June 2009 were:

Ted Levine, the business manager for ice-cream products, is pleased that more pounds of ice cream were sold than budgeted and that revenues were up. Unfortunately, variable manufacturing costs went up too.

The bottom line is that contribution margin declined by $30,000, which is less than 1% of the budgeted revenues of $3,250,000. Overall, Levine feels that the business is running fine.

If you want to use Excel to solve this exercise, go to the Excel Lab at www.prenhall.com/horngrencost13e and download the template for Exercise 7-20.

1. Calculate the static-budget variance in units, revenues, variable manufacturing costs, and contribution margin? What percentage is each static-budget variance relative to its static-budget amount?

2. Break down each static-budget variance into a flexible-budget variance and a sales-volume variance.

3. Calculate the selling-price variance.

4. Assume the role of management accountant at Marron. How would you present the results to Ted Levine? Should he be more concerned? If so why?

Step by Step Answer:

Flexible budget and sales volume variances 1 and 2 3 The selling price variance caused solely by the difference in actual and budgeted selling price i...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0136126638

13th Edition

Authors: Charles T. Horngren, Srikant M.Dater, George Foster, Madhav