Gelato Corporation, a private entity reporting under ASPE, was incorporated on January 3, 2013. The corporation's financial

Question:

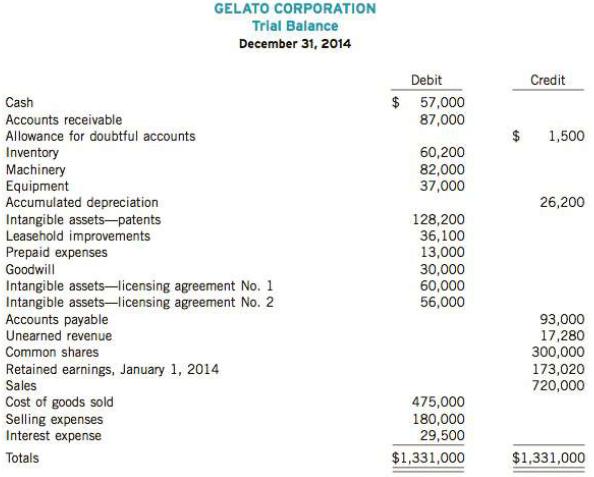

Gelato Corporation, a private entity reporting under ASPE, was incorporated on January 3, 2013. The corporation's financial statements for its first year of operations were not examined by a public accountant. You have been engaged to audit the financial statements for the year ended December 31, 2014, and your audit is almost complete. The corporation’s trial balance is as follows:

The following information is for accounts that may still need adjustment:

1. Patents for Gelato's manufacturing process were acquired on January 2, 2014, at a cost of $87,500. An additional $35,000 was spent in July 2014 and $5,700 in December 2014 to improve machinery covered by the patents and was charged to the Intangible Assets- Patents account. Depreciation on fixed assets was properly recorded for 2014 in accordance with Gelato\; practice, which is to take a full year of depreciation for property on hand at June 30. No other depreciation or amortization was recorded. Gelato uses the straight-line method for all amortization and amortizes its patents over their legal life, which was 17 years when the patent was granted. Accumulate all amortization expense in one income statement account.

2. At December 31, 2014, management determined that the undiscounted future net cash flows that are expected from the use of the patent would be $80,000, the value in use was $75,000, the resale value of the patent was approximately $55,000, and disposal costs would be $5,000.

3. On January 3, 2013, Gelato purchased licensing agreement no. 1, which management believed had an unlimited useful life. Licences similar to this are frequently bought and sold. Gelato could only clearly identify cash flows from agreement no. 1 for 15 years. After the 15 years, further cash flows are still possible, but are uncertain. The balance in the Licenses account includes the agreement’s purchase price of $57,000 and expenses of $3,000 related to the acquisition. On January 1, 2014, Gelato purchased licensing agreement no. 2, which has a life expectancy of

five years. The balance in the Licenses account includes its $54,000 purchase price and $6,000 in acquisition expenses, but it has been reduced by a credit of $4,000 for the advance collection of 2015 revenue from the agreement. In late December 2013, an explosion caused a permanent 60% reduction in the expected revenue-producing value of licensing agreement no. 1. In January 2015, a flood caused additional damage that rendered the agreement worthless.

4. The balance in the Goodwill account results from legal expenses of $30,000 that were incurred for Gelato's incorporation on January 3, 2013. Management assumes that the $30,000 cost will benefit the entire life of the organization, and believes that these costs should be amortized over a limited life of 30 years. No entry has been made yet.

5. The Leasehold Improvements account includes the following: (a) There is a $ 15,000 cost of improvements that Gelato made to premises that it leases as a tenant. The improvements were made in January 2013 and have a useful life of 12 years. (b) Movable assembly-line equipment costing $ 15,000 was installed in the leased premises in December 2014. (c) Real estate taxes of$6,100 were paid by Gelato in 2014, but they should have been paid by the landlord under the terms of the lease agreement. Gelato paid its rent in full during 2014. A 10-year non-renewable lease was signed on January 3, 2013, for the leased building that Gelato uses in manufacturing operations. No amortization or depreciation has been recorded on any amounts related to the lease or improvements.

6. Included in selling expenses are the following costs incurred to develop a new product. Gelato hopes to establish the technical, financial, and commercial viability of this project in fiscal 2015.

Salaries of two employees who spend approximately 50% of their time on research and development initiatives (this amount represents their full salary) ……….. $110,000

Materials consumed ……………………………………………………… 35,000

Instructions

(a) Prepare an eight-column work sheet to adjust the accounts that require adjustment and include columns for an income statement and a statement of financial position. A separate account should be used for the accumulation of each type of amortization. Formal adjusting journal entries and financial statements are not required.

(b) Prepare Gelato's statement of financial position and income statement for the year ended December 31, 2014, in proper form.

(c) Explain how the accounting would differ if Gelato were reporting under IFRS.

Financial StatementsFinancial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial...

Step by Step Answer:

a Gelato Corporation Year Ended December 31 2014 Adjusting Journal Entries Not required 1 Machinery 40700 Intangible Assets Patents 40700 To transfer cost of improving machinery to a PPE account 2 Amo...View the full answer

Intermediate Accounting

ISBN: 978-0176509736

10th Canadian Edition, Volume 1

Authors: Donald Kieso, Jerry Weygandt, Terry Warfield, Nicola Young,