In addition to the five factors discussed in the chapter, dividends also affect the price of an

Question:

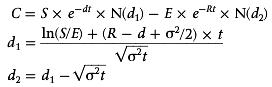

In addition to the five factors discussed in the chapter, dividends also affect the price of an option. The Black€“Scholes option pricing model with dividends is

All of the variables are the same as the Black€“Scholes model without dividends except for the variable d, which is the continuously compounded dividend yield on the stock.

a. What effect do you think the dividend yield will have on the price of a call option? Explain.

b. A stock is currently priced at $93 per share; the standard deviation of its return is 50 percent per year; and the risk-free rate is 5 percent per year, compounded continuously. What is the price of a call option with a strike price of $90 and a maturity of six months if the stock has a dividend yield of 2 percent per year?

Strike PriceIn finance, the strike price of an option is the fixed price at which the owner of the option can buy, or sell, the underlying security or commodity. Dividend

A dividend is a distribution of a portion of company’s earnings, decided and managed by the company’s board of directors, and paid to the shareholders. Dividends are given on the shares. It is a token reward paid to the shareholders for their... Maturity

Maturity is the date on which the life of a transaction or financial instrument ends, after which it must either be renewed, or it will cease to exist. The term is commonly used for deposits, foreign exchange spot, and forward transactions, interest...

Step by Step Answer:

a Going back to the chapter on dividends the price of th...View the full answer

Corporate Finance

ISBN: 978-0071339575

7th Canadian Edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Gordon Ro