Items a through l represent possible errors and fraud that you suspect may be present at Rex

Question:

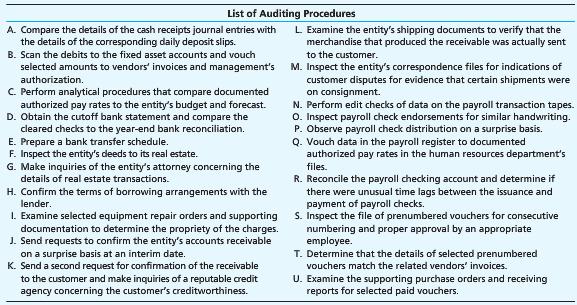

Items a through l represent possible errors and fraud that you suspect may be present at Rex Company. The accompanying List of Auditing Procedures represents procedures that the auditor would consider performing to gather evidence concerning possible errors and fraud. For each item, select one or two procedures, as indicated, that the auditor most likely would perform to gather evidence in support of that item. The procedures on the list may be selected once, more than once, or not at all.

Possible Misstatements

a. The auditor suspects that a kiting scheme exists because an accounting department employee who can issue and record checks seems to be leading an unusually luxurious lifestyle. (Select only 1 procedure.)

b. An auditor suspects that the controller wrote several checks and recorded the cash disbursements just before year-end but did not mail the checks until after the first week of the subsequent year. (Select only 1 procedure.)

c. The entity borrowed funds from a financial institution. Although the transaction was properly recorded, the auditor suspects that the loan created a lien on the entity’s real estate that is not disclosed in its financial statements. (Select only 1 procedure.)

d. The auditor discovered an unusually large receivable from one of the entity’s new customers. The auditor suspects that the receivable may be fictitious because the auditor has never heard of the customer and because the auditor’s initial attempt to confirm the receivable has been ignored by the customer. (Select only 2 procedures.)

e. The auditor suspects that fictitious employees have been placed on the payroll by the entity’s payroll supervisor, who has access to payroll records and to the paychecks. (Select only 1 procedure.)

f. The auditor suspects that selected employees of the entity received unauthorized raises from the entity’s payroll supervisor, who has access to payroll records. (Select only 1 procedure.)

g. The entity’s cash receipts of the first few days of the subsequent year were properly deposited in its general operating account after the year-end. However, the auditor suspects that the entity recorded the cash receipts in its books during the last week of the year under audit. (Select only 1 procedure.)

h. The auditor suspects that vouchers were prepared and processed by an accounting department employee for merchandise that was neither ordered nor received by the entity.

(Select only 1 procedure.)

i. The details of invoices for equipment repairs were not clearly identified or explained to the accounting department employees. The auditor suspects that the bookkeeper incorrectly recorded the repairs as fixed assets. (Select only 1 procedure.)

j. The auditor suspects that a lapping scheme exists because an accounting department employee who has access to cash receipts also maintains the accounts receivable ledger and refuses to take any vacation or sick days. (Select only 2 procedures.)

k. The auditor suspects that the entity is inappropriately increasing the cash reported on its balance sheet by drawing a check on one account and not recording it as an outstanding check on that account and simultaneously recording it as a deposit in a second account. (Select only 1 procedure.)

l. The auditor suspects that the entity’s controller has overstated sales and accounts receivable by recording fictitious sales to regular customers in the entity’s books. (Select only 2 procedures.)

Accounts ReceivableAccounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that... Balance Sheet

Balance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial...

Step by Step Answer:

a E Kiting involves manipulations causing an amount of cash to be included simultaneously in the balance of two or more bank accounts Kiting schemes a...View the full answer

Principles of Auditing and Other Assurance Services

ISBN: 978-0078025617

19th edition

Authors: Ray Whittington, Kurt Pany