Jumping Juice Ltd. produces two grades of sparkling apple juice. A diagram of the production process appears

Question:

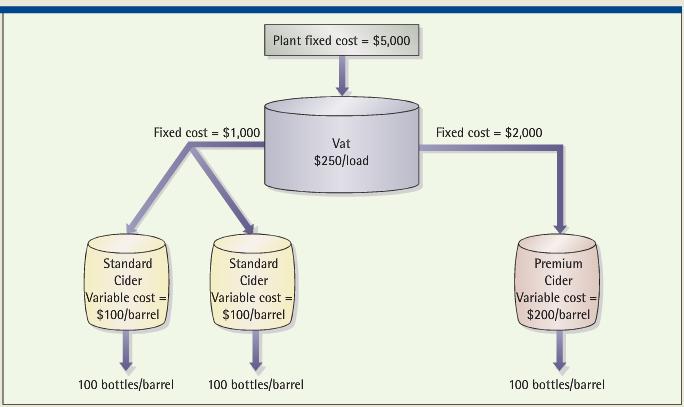

Jumping Juice Ltd. produces two grades of sparkling apple juice. A diagram of the production process appears in Exhibit 9.6. The process begins when the vat is loaded with apples. The incremental cost of raw materials and processing one load is $250. Each load produces one barrel of premium raw apple juice and two barrels of standard raw apple juice. The variable cost of carbonating and bottling the cider is $200 per barrel for premium cider and $100 per barrel for standard cider. Each barrel of raw juice produces 100 bottles of finished sparkling juice. The fixed costs for one month are: $5,000 for the plant, $2,000 for handling and bottling premium, and $1,000 for handling and bottling standard. Premium cider sells for $5 per bottle and standard cider for $3 per bottle, both wholesale. In a normal month, 100 loads are processed and converted into 20,000 bottles of standard cider and 10,000 bottles of premium cider.

A. In a normal month, what is the total allocated cost (fixed plus variable) per bottle of premium cider if the costs of the manufacturing operation are allocated on the basis of physical output measured by volume?

B. In a normal month, what is the variable cost per bottle of premium cider if the joint variable costs of the juice company are allocated on the basis of physical output measured by volume?

C. Assuming that the $1,000 in fixed costs for standard handling and bottling could be avoided, what would be the impact on the profit of the company in a normal month if the company discontinued the standard brand and treated all raw cider as premium grade?

D. Explain to the CEO of the company why the variable cost per bottle of premium cider you calculated in part (B) should or should not be used in pricing special orders for the premium cider.

Step by Step Answer:

A According to the requirements of the problem the costs of the vat process need to be allocated whi...View the full answer

Cost Management Measuring Monitoring and Motivating Performance

ISBN: 978-0470769423

2nd edition

Authors: Leslie G. Eldenburg, Susan K. Wolcott