Kazuo Piano Company has two producing departments, traditional pianos and electronic pianos. In addition, there are two

Question:

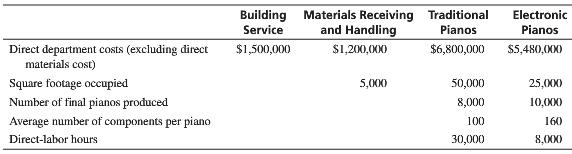

Kazuo Piano Company has two producing departments, traditional pianos and electronic pianos. In addition, there are two service departments, building services and materials receiving and handling. The company purchases a variety of component parts from which the departments assemble pianos for sale in domestic and international markets.

The electronic pianos division is highly automated. The manufacturing costs depend primarily on the number of subcomponents in each piano. In contrast, the traditional pianos division relies primarily on a large labor force to hand-assemble pianos. Its costs depend on direct-labor hours.

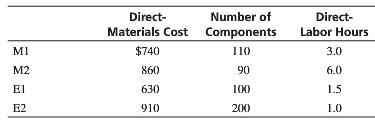

The costs of building services depend primarily on the square footage occupied. The costs of materials receiving and handling depend primarily on the total number of components handled. Pianos M1 and M2 are produced in the traditional pianos department, and E1 and E2 are produced in the electronic pianos department. Data about these products follow:

Budget figures for 20X7 include the following:

1. Allocate the costs of the service departments using the direct method.

2. Using the results of number 1, compute the cost per direct-labor hour in the traditional pianos department and the cost per component in the electronic pianos department.

3. Using the results of number 2, compute the cost per unit of product for pianos M1, M2, E1, and E2.

Step by Step Answer:

1 Calculations 50000 25000 75000 50000 75000 1500000 1000000 25000 75000 1500000 500000 No ...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta