Leather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part

Question:

Leather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part of the United States. Foreign competition has forced its owner, Heather Gray, to explore new ways to meet the competition. One of her cousins, Wallace Hayes, who recently graduated from college with a major in accounting, told her about the use of cost variance analysis to learn about efficiencies of production. In May 2014, Heather asked Matt Jones, chief accountant, and Alfred Prudest, production manager, to implement a standard costing system. Matt and Alfred, in turn, retained Shannon Leikam, an accounting professor at Harding’s College, to set up a standard costing system by using information supplied to her by Matt’s and Alfred’s staff. To verify that the information was accurate, Shannon visited the plant and measured workers’ output using time and motion studies. During those visits, she was not accompanied by either Matt or Alfred, and the workers knew about Shannon’s schedule in advance. The cost system was implemented in June 2014. Recently, the following dialogue took place among Heather, Matt, and Alfred:

HEATHER: How is the business performing?

ALFRED: You know, we are producing a lot more than we used to, thanks to the contract that you helped obtain from Lean, Inc., for laptop covers. (Lean is a national supplier of computer accessories.)

MATT: Thank goodness for that new product. It has kept us from sinking even more due to the inroads into our business made by those foreign suppliers of leather goods.

HEATHER: What about the standard costing system?

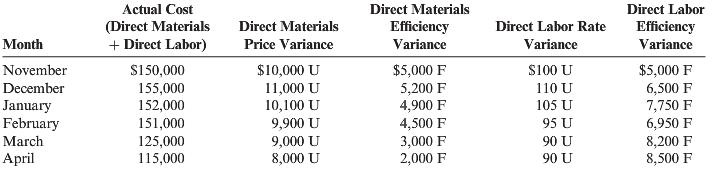

MATT: The variances are mostly favorable, except for the first few months when the supplier of leather started charging more.

HEATHER: How did the union members take to the standards?

ALFRED: Not bad. They grumbled a bit at first, but they have taken it in stride. We’ve consistently shown favorable direct labor efficiency variances and direct materials usage variances. The direct labor rate variance has been flat.

MATT: It should be since direct labor rates are negotiated by the union representative at the start of the year and remain the same for the entire year.

HEATHER: Matt, would you send me the variance report for laptop covers immediately? The following chart summarizes the direct materials and direct labor variances from November 2014 through April 2015 (extracted from the report provided by Matt). Standards for each laptop cover are as follows:

a. Three feet of direct materials at $7.50 per foot

b. Forty five minutes of direct labor at $14 per hour

In addition, the data for May 2015, but not the variances for the month, are as follows:

Laptop covers made in May………………………………… 2,900 units

Total actual direct materials costs incurred………………… $ 68,850

Actual quantity of direct materials purchased and used…… 8,500 feet

Total actual direct labor cost incurred ……………………. $ 25,910

Total actual direct labor hours……………………………. 1,837.6 hours

Actual direct labor cost per hour exceeded the budgeted rate by $0.10 per hour.

Required:

1. For May 2015, calculate the price and quantity variances for direct labor and direct materials.

2. Discuss the trend of the direct materials and labor variances.

3. What type of actions must the workers have taken during the period they were being observed for the setting of standards?

4. What can be done to ensure that the standards are set correctly? (CMA adapted)

Step by Step Answer:

1 MPV AP SP AQ 810 7508500 5100 U MUV AQ SQ SP 8500 8700750 1500 F where SQ 3 2900 LRV AR SR AH 1410 140018376 18376 U where SH 4560 2900 LEV AH SH SR ...View the full answer

Cornerstones of Cost Management

ISBN: 978-1285751788

3rd edition

Authors: Don R. Hansen, Maryanne M. Mowen