MacDonalds Highland Shoppe Ltd. (MHS) imports top quality kilts and accessories directly from Scotland for sale to

Question:

MacDonald€™s Highland Shoppe Ltd. (MHS) imports top quality kilts and accessories directly from Scotland for sale to Canadian and American customers. Because of its international suppliers and customers, MHS uses IFRS.

It is October 18, 2013, and on November 1, 2013, MHS plans to enter into a firm commitment to purchase inventory from a supplier in Scotland for £100,000. Payment is to be made upon delivery of the inventory on February 28, 2013. Because of uncertain foreign currency markets, the owner-manager, Mac, is considering entering into a forward contract to hedge the currency risk but is uncertain how this will affect the financial statements. He wants you, the company accountant, to determine the effect of these transactions on MHS€™s 2013 and 2014 income statements (year end is December 31) under the following assumptions:

1. On November 1, 2013, MHS enters into a forward contract with a bank to buy £100,000 at the four-month forward rate.

2. The payment to the supplier is made on February 28, 2014.

3. All the inventory obtained in this purchase is sold in 2014.

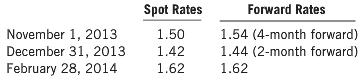

Mac would like you to use the following assumed exchange rates in your calculations:

Mac would also like you to provide some information about hedge accounting, so the company can make an informed decision on whether or not to use this approach.

Required

(a) Calculate the effect of exchange rate changes for the above scenario on MHS 2013 and 2014 income statements, assuming that hedge accounting is not used. Your calculations should include both the income effect of exchange gains and losses and cost of goods sold. Ignore income taxes.

(b) Explain how hedge accounting would avoid the income statement effects calculated in part (a) assuming that the forward contract is designated as a cash flow hedge.

The value of one currency for the purpose of conversion to another. Exchange Rate means on any day, for purposes of determining the Dollar Equivalent of any currency other than Dollars, the rate at which such currency may be exchanged into Dollars...

Step by Step Answer:

a The effect of exchange rate changes on MHS for the 2013 and 2014 income statement assuming that he...View the full answer