Monster Toys is considering a new toy monster called Garga. Annual sales of Garga are estimated at

Question:

Monster Toys is considering a new toy monster called Garga. Annual sales of Garga are estimated at 100,000 units at a price of $8 per unit. Variable manufacturing costs are estimated at $3 per unit, incremental fixed manufacturing costs (excluding depreciation) at $60,000 annually, and additional selling and general expenses related to the monsters at $40,000 annually.

To manufacture the monsters, the company must invest $400,000 in design molds and special equipment. Since toy fads wane in popularity rather quickly, Monster Toys anticipates the special equipment will have a three-year service life with only a $10,000 salvage value. Depreciation will be computed on a straight-line basis. All revenue and expenses other than depreciation will be received or paid in cash. The company’s combined federal and state income tax rate is 30 percent.

Instructions

a. Prepare a schedule showing the estimated increase in annual net income from the planned manufacture and sale of Garga.

b. Compute the annual net cash flows expected from this project.

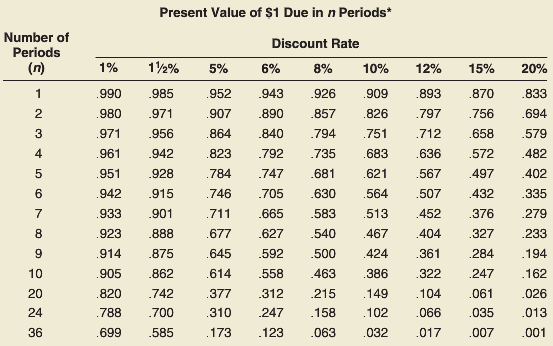

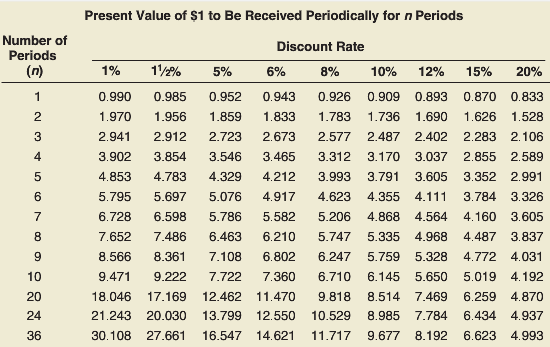

c. Compute for this project the (1) payback period, (2) return on average investment, and (3) net present value, discounted at an annual rate of 12 percent. Round the payback period to the nearest tenth of a year and the return on average investment to the nearest tenth of a percent. Use Exhibits 26–3 and 26–4 where necessary.

In Exhibits 26–3

In Exhibits 26–4

What is NPV? The net present value is an important tool for capital budgeting decision to assess that an investment in a project is worthwhile or not? The net present value of a project is calculated before taking up the investment decision at... Salvage Value

Salvage value is the estimated book value of an asset after depreciation is complete, based on what a company expects to receive in exchange for the asset at the end of its useful life. As such, an asset’s estimated salvage value is an important... Payback Period

Payback period method is a traditional method/ approach of capital budgeting. It is the simple and widely used quantitative method of Investment evaluation. Payback period is typically used to evaluate projects or investments before undergoing them,...

Step by Step Answer:

a MONSTER TOYS Schedule of Estimated Net Income Estimated sales 100000 units 8 800000 Less estimated ...View the full answer

Financial and Managerial Accounting the basis for business decisions

ISBN: 978-0078111044

16th edition

Authors: Jan Williams, Susan Haka, Mark Bettner, Joseph Carcello