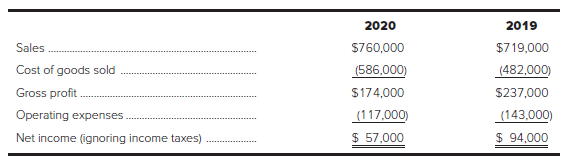

Following are condensed income statements for Uncle Bill?s Home Improvement Center for the years ended December 31,

Question:

Following are condensed income statements for Uncle Bill?s Home Improvement Center for the years ended December 31, 2020 and 2019:

Uncle Bill was concerned about the operating results for 2020 and asked his recently hired accountant, ?If sales increased in 2020, why was net income so much less than what it was in 2019?? In February of 2021, Uncle Bill got his answer: ?The ending inventory reported in 2019 was overstated by $30,000 for merchandise that we were holding on consignment on behalf of Kirk?s Servistar. We still keep some of their appliances in stock, but the value of these items was not included in the 2020 inventory count because we don?t own them.?

a. Recast the 2019 and 2020 income statements to take into account the correction of the 2019 ending inventory error.

b. Calculate the combined net income for 2019 and 2020 before and after the correction of the error. Explain to Uncle Bill why the error was corrected in 2020 before it was actually discovered in 2021.

c. What effect, if any, will the error have on net income and stockholders? equity in 2021?

Ending InventoryThe ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =...

Step by Step Answer:

a 2020 2019 Sales 760000 719000 Cost of goods sold 556000 512000 Gross profit 204000 207000 Operatin...View the full answer

Accounting What the Numbers Mean

ISBN: 978-1260565492

12th edition

Authors: David Marshall, Wayne McManus, Daniel Viele