After testing internal controls, Leigh and Rory have come to the conclusion that most of Crest Outfitters

Question:

After testing internal controls, Leigh and Rory have come to the conclusion that most of Crest Outfitters’ controls are operating as designed, though they did encounter some issues around the end of the financial year when staff not from the warehouse and logistics area helped pack orders due to large volumes of sales. Crest Outfitters offers big discounts in June and this results in a surge in transactions. Staff from all different parts of the company come together to help get these orders shipped in time for Crest to recognise the revenue in the current financial year.

As a result of the conclusion that controls are working effectively, Rory and Leigh now turn to the substantive testing phase of the audit. Leigh has been learning about using more automated tools and techniques in her audit and assurance subject at university and asks Rory about using more substantive analytical procedures.

Rory tells Leigh, ‘Our testing must respond to the risk of material misstatement at the assertion level. For each assertion, the audit team determines the level of detection risk, which is based on the inherent risk assessment and the results of the control testing, which is used to establish the level of control risk. The auditors also have to consider a range of practical factors, such as constraints on timing and the complexity of the client’s systems. Analytical procedures are always useful, but the decision to use analytical procedures and/or other substantive procedures must consider risk and practical factors’, he says. ‘In an audit we have to decide what an acceptable level of detection risk is, and how to achieve it, for every assertion about transactions, account balances and disclosures. Will analytical procedures allow us to collect evidence on all of the relevant assertions at once?’

Leigh realises that she’s going to need to collect persuasive evidence on all of the assertions related to sales (and cash), and analytical procedures may not provide her with sufficient and appropriate evidence. Sales is an account of great importance to the financial statements — it is material purely in its size but also qualitatively important because without sales, Crest Outfitters would not be a going concern.

Rory explains further about substantive analytical procedures. ‘Using analytical procedures as the only substantive procedure is more appropriate if we can find a close relationship between the underlying activity data and the account balance. The weaker or less consistent the relationship between the account balance and the other data, the more likely it is that we’ll have to perform other substantive procedures in order to obtain sufficient and appropriate evidence.’

Leigh thinks for moment, and says, ‘I’ve just realised — when we’re using prior-year data we know it’s audited, but the current year’s trial balance is as yet unaudited. This means we need to recognise that there could be errors in those figures. Also, as we do the audit and we find and correct misstatements, we should have another look at our analytical procedures — the change in the underlying data might change our conclusions!’

‘That’s right,’ says Rory. ‘We might also discover a change in conditions, such as an operational change, that could affect our interpretation of the data. We have to be aware of how everything’s connected and review our conclusions and decisions as we go through the audit. If we can get persuasive evidence from using analytical procedures, we can reduce the reliance on the other substantive tests.’

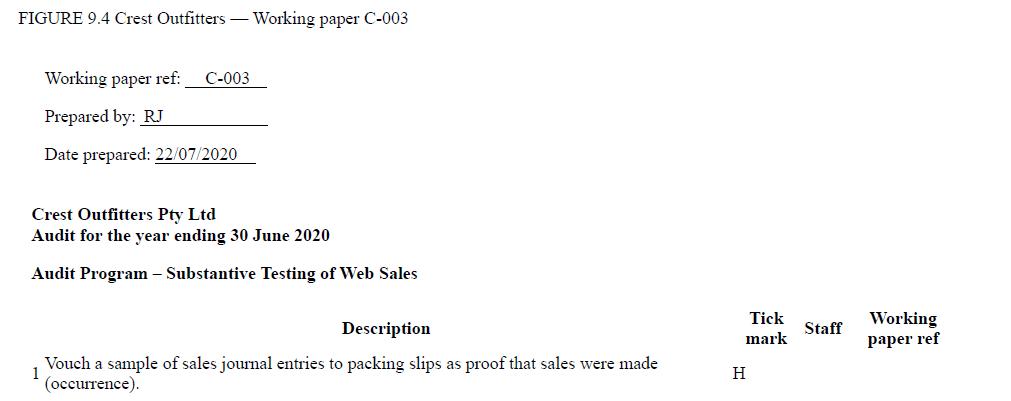

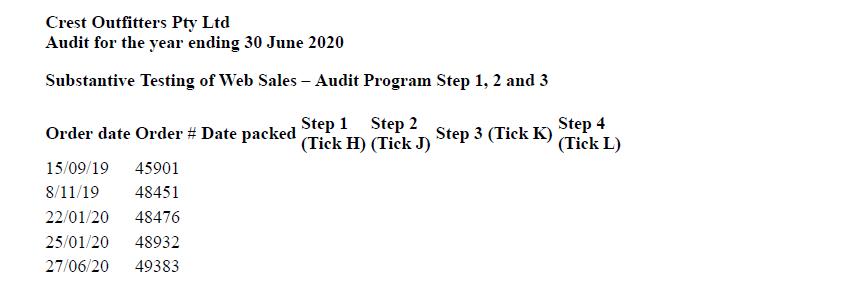

Rory has prepared the following audit program (figure 9.4) to substantively test sales made via Crest’s website. In this exercise, you are in the role of Leigh and your job is to complete steps 1, 2, 3 and 4 using the evidence supplied by the client. You’ve been given working paper C-004 in figure 9.5 to document the findings.

Required

(a) Are sales from the website materially misstated?

(b) Should this be the conclusion of the substantive testing over web sales? Have all of the relevant assertions been tested?

Step by Step Answer:

Auditing A Practical Approach

ISBN: 9780730382645

4th Edition

Authors: Robyn Moroney, Fiona Campbell, Jane Hamilton