Question:

Refer to Exhibit 2.8. The Sarbanes-Oxley Act enacted which of the following provisions relevant to auditors and the audit opinion formulation process?

a. The PCAOB was established, and it has the power to conduct inspections of public company audits.

b. The lead audit partner and reviewing partner must rotate off the audit of a publicly traded company at least every ten years.

c. In the annual report, management must acknowledge that they are required to have the company’s internal audit function attest to the accuracy of the annual reports.

d. All of the above.

e. None of the above.

Transcribed Image Text:

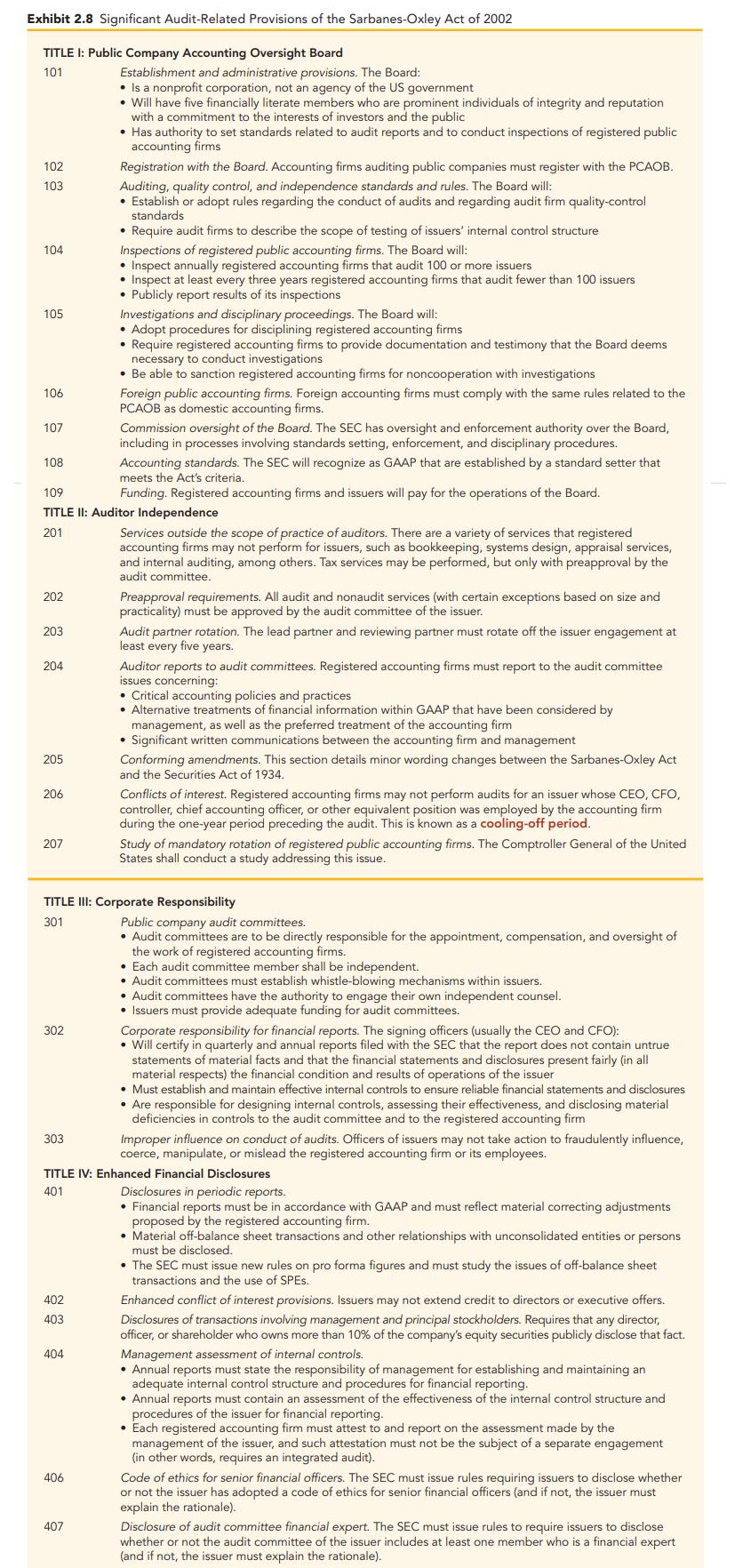

Exhibit 2.8 Significant Audit-Related Provisions of the Sarbanes-Oxley Act of 2002

TITLE I: Public Company Accounting Oversight Board

101

102

103

104

105

106

107

108

202

203

204

205

206

109

TITLE II: Auditor Independence

201

207

302

303

402

403

Establishment and administrative provisions. The Board:

• Is a nonprofit corporation, not an agency of the US government

• Will have five financially literate members who are prominent individuals of integrity and reputation

with a commitment to the interests of investors and the public

404

• Has authority to set standards related to audit reports and to conduct inspections of registered public

accounting firms

406

Registration with the Board. Accounting firms auditing public companies must register with the PCAOB.

Auditing, quality control, and independence standards and rules. The Board will:

• Establish or adopt rules regarding the conduct of audits and regarding audit firm quality-control

standards.

• Require audit firms to describe the scope of testing of issuers' internal control structure

Inspections of registered public accounting firms. The Board will:

• Inspect annually registered accounting firms that audit 100 or more issuers

• Inspect at least every three years registered accounting firms that audit fewer than 100 issuers

• Publicly report results of its inspections

407

Investigations and disciplinary proceedings. The Board will:

• Adopt procedures for disciplining registered accounting firms

• Require registered accounting firms to provide documentation and testimony that the Board deems

necessary to conduct investigations

• Be able to sanction registered accounting firms for noncooperation with investigations

Foreign public accounting firms. Foreign accounting firms must comply with the same rules related to the

PCAOB as domestic accounting firms.

Commission oversight of the Board. The SEC has oversight and enforcement authority over the Board,

including in processes involving standards setting, enforcement, and disciplinary procedures.

Accounting standards. The SEC will recognize as GAAP that are established by a standard setter that

meets the Act's criteria..

Funding. Registered accounting firms and issuers will pay for the operations of the Board.

Services outside the scope of practice of auditors. There are a variety of services that registered

accounting firms may not perform for issuers, such as bookkeeping, systems design, appraisal services,

and internal auditing, among others. Tax services may be performed, but only with preapproval by the

audit committee.

Preapproval requirements. All audit and nonaudit services (with certain exceptions based on size and

practicality) must be approved by the audit committee of the issuer.

Audit partner rotation. The lead partner and reviewing partner must rotate off the issuer engagement at

least every five years.

TITLE III: Corporate Responsibility

301

Auditor reports to audit committees. Registered accounting firms must report to the audit committee

issues concerning:

• Critical accounting policies and practices

• Alternative treatments of financial information within GAAP that have been considered by

management, as well as the preferred treatment of the accounting firm

• Significant written communications between the accounting firm and management

Conforming amendments. This section details minor wording changes between the Sarbanes-Oxley Act

and the Securities Act of 1934.

Conflicts of interest. Registered accounting firms may not perform audits for an issuer whose CEO, CFO,

controller, chief accounting officer, or other equivalent position was employed by the accounting firm

during the one-year period preceding the audit. This is known as a cooling-off period.

Study of mandatory rotation of registered public accounting firms. The Comptroller General of the United

States shall conduct a study addressing this issue.

Public company audit committees.

• Audit committees are to be directly responsible for the appointment, compensation, and oversight of

the work of registered accounting firms.

TITLE IV: Enhanced Financial Disclosures

401

Disclosures in periodic reports.

• Financial reports must be in accordance with GAAP and must reflect material correcting adjustments

proposed by the registered accounting firm.

• Each audit committee member shall be independent.

• Audit committees must establish whistle-blowing mechanisms within issuers.

• Audit committees have the authority to engage their own independent counsel.

• Issuers must provide adequate funding for audit committees.

Corporate responsibility for financial reports. The signing officers (usually the CEO and CFO):

• Will certify in quarterly and annual reports filed with the SEC that the report does not contain untrue

statements of material facts and that the financial statements and disclosures present fairly (in all

material respects) the financial condition and results of operations of the issuer

• Must establish and maintain effective internal controls to ensure reliable financial statements and disclosures

• Are responsible for designing internal controls, assessing their effectiveness, and disclosing material

deficiencies in controls to the audit committee and to the registered accounting firm

Improper influence on conduct of audits. Officers of issuers may not take action to fraudulently influence,

coerce, manipulate, or mislead the registered accounting firm or its employees.

• Material off-balance sheet transactions and other relationships with unconsolidated entities or persons

must be disclosed.

• The SEC must issue new rules on pro forma figures and must study the issues of off-balance sheet

transactions and the use of SPES.

Enhanced conflict of interest provisions. Issuers may not extend credit to directors or executive offers.

Disclosures of transactions involving management and principal stockholders. Requires that any director,

officer, or shareholder who owns more than 10% of the company's equity securities publicly disclose that fact.

Management assessment of internal controls.

• Annual reports must state the responsibility of management for establishing and maintaining an

adequate internal control structure and procedures for financial reporting.

• Annual reports must contain an assessment of the effectiveness of the internal control structure and

procedures of the issuer for financial reporting.

• Each registered accounting firm must attest to and report on the assessment made by the

management of the issuer, and such attestation must not be the subject of a separate engagement

(in other words, requires an integrated audit).

Code of ethics for senior financial officers. The SEC must issue rules requiring issuers to disclose whether

or not the issuer has adopted a code of ethics for senior financial officers (and if not, the issuer must

explain the rationale).

Disclosure of audit committee financial expert. The SEC must issue rules to require issuers to disclose

whether or not the audit committee of the issuer includes at least one member who is a financial expert

(and if not, the issuer must explain the rationale).