Question:

Consider Figure 12-13, where a substantive analysis of inventory turnover was performed during the audit of Jones Manufacturing Company to determine whether inventory should be written down due to obsolescence.

a. Is the total proposed adjustment material? What factors go into your judgment?

b. What factors may need further consideration before the auditor argues for a writedown on item no. J665?

c. What arguments could Jones Manufacturing's management advance to defend against an obsolescence write-down?

Figure 12-13

Transcribed Image Text:

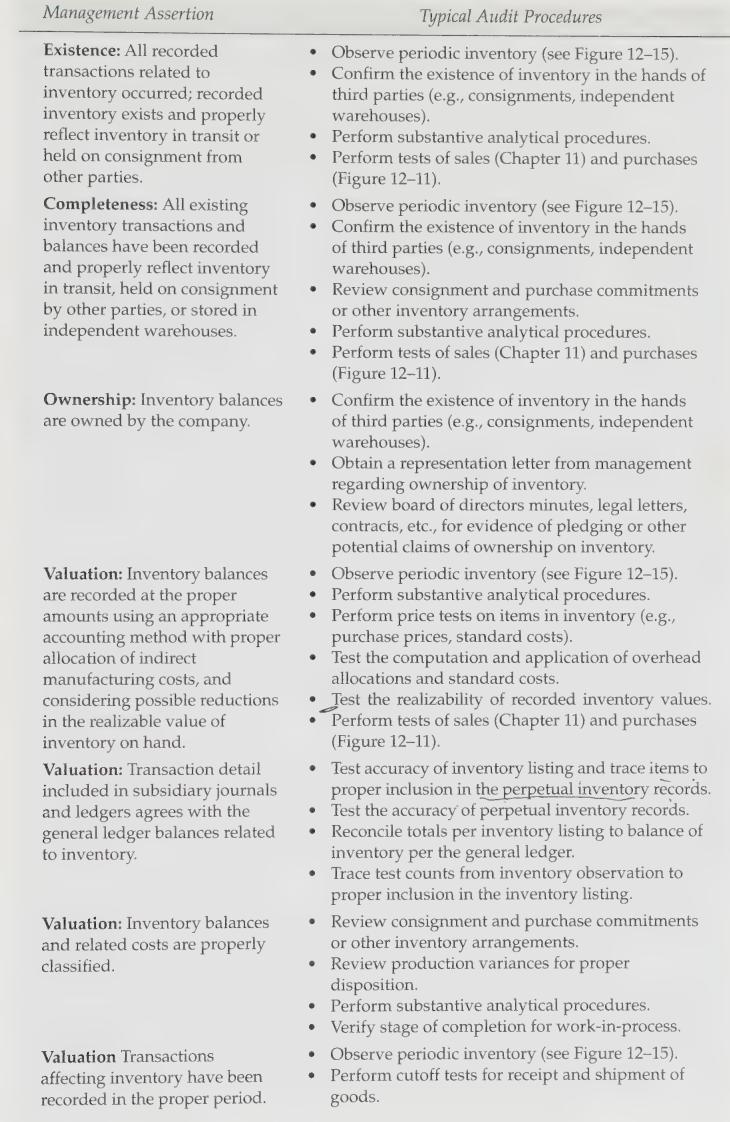

Management Assertion Existence: All recorded transactions related to inventory occurred; recorded inventory exists and properly reflect inventory in transit or held on consignment from other parties. Completeness: All existing inventory transactions and balances have been recorded and properly reflect inventory in transit, held on consignment by other parties, or stored in independent warehouses. Ownership: Inventory balances are owned by the company. Typical Audit Procedures Observe periodic inventory (see Figure 12-15). Confirm the existence of inventory in the hands of third parties (eg, consignments, independent warehouses). Perform substantive analytical procedures. Perform tests of sales (Chapter 11) and purchases (Figure 12-11). Observe periodic inventory (see Figure 12-15). Confirm the existence of inventory in the hands of third parties (e.g., consignments, independent warehouses). Review consignment and purchase commitments or other inventory arrangements. Perform substantive analytical procedures. Perform tests of sales (Chapter 11) and purchases (Figure 12-11). Confirm the existence of inventory in the hands of third parties (e.g. consignments, independent warehouses). Obtain a representation letter from management regarding ownership of inventory. Review board of directors minutes, legal letters, contracts, etc., for evidence of pledging or other potential claims of ownership on inventory. Valuation: Inventory balances are recorded at the proper amounts using an appropriate accounting method with proper allocation of indirect manufacturing costs, and considering possible reductions in the realizable value of inventory on hand. Valuation: Transaction detail included in subsidiary journals and ledgers agrees with the general ledger balances related to inventory. Valuation: Inventory balances and related costs are properly classified. Valuation Transactions affecting inventory have been recorded in the proper period. Observe periodic inventory (see Figure 12-15). Perform substantive analytical procedures. Perform price tests on items in inventory (e.g., purchase prices, standard costs). Test the computation and application of overhead allocations and standard costs. Test the realizability of recorded inventory values. Perform tests of sales (Chapter 11) and purchases (Figure 12-11). Test accuracy of inventory listing and trace items to proper inclusion in the perpetual inventory records. Test the accuracy of perpetual inventory records. Reconcile totals per inventory listing to balance of inventory per the general ledger. Trace test counts from inventory observation to proper inclusion in the inventory listing. Review consignment and purchase commitments or other inventory arrangements. Review production variances for proper disposition. Perform substantive analytical procedures. Verify stage of completion for work-in-process. Observe periodic inventory (see Figure 12-15). Perform cutoff tests for receipt and shipment of goods.