Question:

Public accounting firms and regulators have long been concerned with the notion of the "expectations gap," which describes an accounting firm's understanding of the assertions provided in an auditor's report compared to the users' understanding of those assertions. Consider the form and content of a standard unqualified auditor's report (e.g., Figure 15-8). Surveys regarding what users believe is conveyed in an opinion suggest that an expectations gap exists. The most serious gap found is a consistent belief by users that they are receiving a guarantee against fraud and errors from the auditor. Based on your review of the standard unqualified report, describe why you believe that this gap persists.

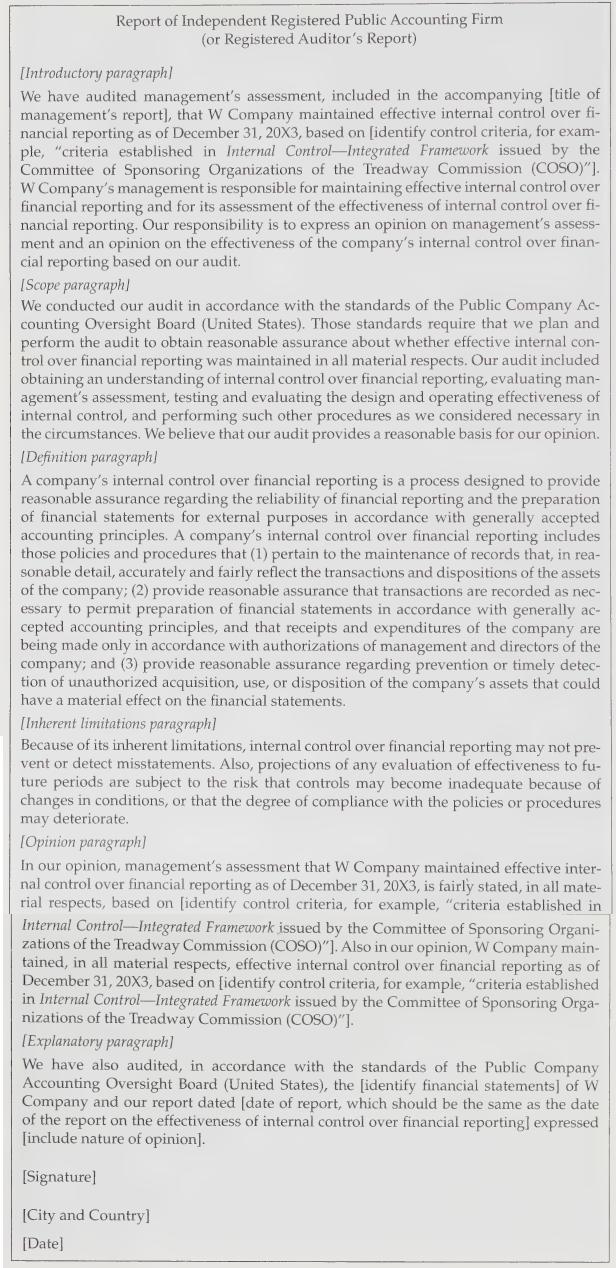

Figure 15-8

Transcribed Image Text:

Report of Independent Registered Public Accounting Firm (or Registered Auditor's Report) [Introductory paragraph] We have audited management's assessment, included in the accompanying [title of management's report], that W Company maintained effective internal control over fi- nancial reporting as of December 31, 20X3, based on [identify control criteria, for exam- ple, "criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO)"]. W Company's management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over fi- nancial reporting. Our responsibility is to express an opinion on management's assess- ment and an opinion on the effectiveness of the company's internal control over finan- cial reporting based on our audit. [Scope paragraph] We conducted our audit in accordance with the standards of the Public Company Ac- counting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal con- trol over financial reporting was maintained in all material respects. Our audit included obtaining an understanding of internal control over financial reporting, evaluating man- agement's assessment, testing and evaluating the design and operating effectiveness of internal control, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. [Definition paragraph] A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in rea- sonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as nec- essary to permit preparation of financial statements in accordance with generally ac- cepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detec- tion of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements. [Inherent limitations paragraph] Because of its inherent limitations, internal control over financial reporting may not pre- vent or detect misstatements. Also, projections of any evaluation of effectiveness to fu- ture periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. [Opinion paragraph] In our opinion, management's assessment that W Company maintained effective inter- nal control over financial reporting as of December 31, 20X3, is fairly stated, in all mate- rial respects, based on [identify control criteria, for example, "criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organi- zations of the Treadway Commission (COSO)"]. Also in our opinion, W Company main- tained, in all material respects, effective internal control over financial reporting as of December 31, 20X3, based on [identify control criteria, for example, "criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Orga- nizations of the Treadway Commission (COSO)"]. [Explanatory paragraph/ We have also audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the [identify financial statements] of W Company and our report dated [date of report, which should be the same as the date of the report on the effectiveness of internal control over financial reporting] expressed [include nature of opinion]. [Signature] [City and Country] [Date]