Burlingham Bees, an independent, minor league baseball team, competes in the Northwest Coast League. The team finished

Question:

Burlingham Bees, an independent, minor league baseball team, competes in the Northwest Coast League. The team finished in second place in 2008 with an 87-57 record. The Bees’ 2008 cumulative season attendance of 434,348 spectators a new record ‘high for the team, up more than 10% from the prior season’s attendance.

Bank-loan covenants require the Bees to submit audited financial statements annually to the bank. The accounting firm of Hickman and Snowden, CPAs, has served as the Bees’ auditor for the past five years.

One of the major audit areas involves testing ticket revenues. Ticket revenues reached nearly $2.2 million in 2007. In 2008 the unaudited ticket revenues are reported to be $2,580,420 with net income before tax of $480,100. In prior years, the audit plan called for extensive detail testing of revenue accounts to gain assurance that reported ticket revenues were fairly stated.

Michelle Kramme, a new,.ajpdit ina.nager, just received the assignment to be the manager on the 2008 audit. Michelle worked previously oil tK'e'B'e’tes’ prior-year audits as a staff auditor. When she learned she would be managing the current-year engagement, she immediately thought back to all the hours of detailed testing of ticket sales she performed. On some of her other clients, Michelle has been successful at redesigning audit plans to make better use of analytical procedures as substantive tests. She is beginning to wonder if there is a more efficient way to gather effective substantive evidence related to ticket revenues on the Bees’ engagement.

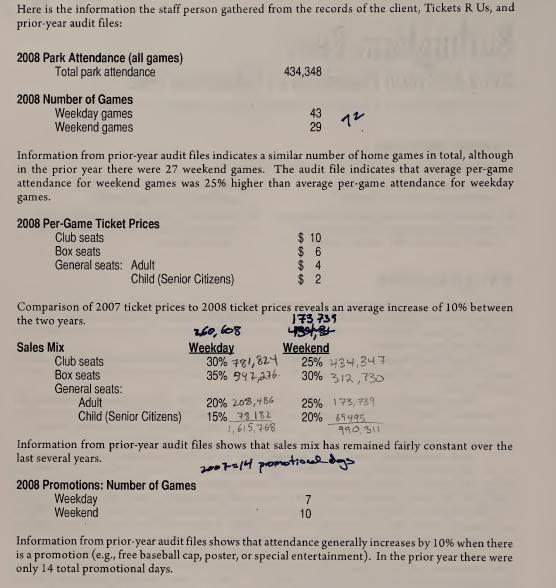

In her first meeting with Bees’ management for the 2008 audit, Michelle learned that the Bees now use an outside company, Tickets R Us, to operate ticket gates for home games. The terms of the contract require Tickets R Us to collect ticket stubs so that it can later report total tickets collected per game. While Tickets R Us does not break down the total ticket sales into the various price categories, Michelle thinks there may be a way to develop an analytical procedure using the independently generated total ticket numbers and data from prior audits. To investigate this possibility, Michelle asked a staff person to gather some information related to reported sales.

REQUIRED [1] Research professional standards (AU329) and list the requirements related to developing an expectation and conducting analytical procedures when those procedures are intended to" provide substantive evidence. What are the advantages of developing an expectation at a detailed level (i.e., using disaggregated data) rather than at an overall or aggregated level?

[2] Using the information provided, please develop a precise expectation (i.e., using the detailed or disaggregated data provided) for ticket revenues for the 2008 fiscal year.

[3]

(a) How close does the Bees’ reported ticket revenue for 2008 have to be to your expectation for you to consider reported ticket revenue reasonable or fairly stated?

(b) If reported ticket revenues were outside your “reasonableness range,” what could explain the difference?

[4]

(a) What are the advantages of using analytical procedures as substantive tests?

(b) If the engagement team decides to use analytical procedures for the Bees’ audit, how will the audit plan differ from prior years?

(c) Discuss whether you believe analytical procedures should be used as substantive tests for the Bees 2008 audit?

Step by Step Answer:

Auditing Cases An Interactive Learning Approach

ISBN: 978-0132423502

4th Edition

Authors: Steven M Glover, Douglas F Prawitt