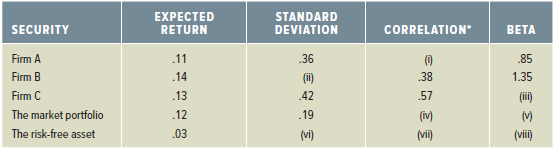

You have been provided the following data on the securities of three firms, the market portfolio, and

Question:

a. Fill in the missing values in the table.

b. Is the stock of Firm A correctly priced according to the capital asset pricing model (CAPM)? What about the stock of Firm B? Firm C? If these securities are not correctly priced, what is your investment recommendation for someone with a well-diversified portfolio?

The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and expected return for assets, particularly stocks. The CAPM is a model for pricing an individual security or portfolio. For individual securities, we make use of the security market line (SML) and its...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a i Using the equation to calculate beta we find I p IM I M 85 p IM 3619 pIM 45 ii Using the equatio...View the full answer

Answered By

Pushpinder Singh

Currently, I am PhD scholar with Indian Statistical problem, working in applied statistics and real life data problems. I have done several projects in Statistics especially Time Series data analysis, Regression Techniques.

I am Master in Statistics from Indian Institute of Technology, Kanpur.

I have been teaching students for various University entrance exams and passing grades in Graduation and Post-Graduation.I have expertise in solving problems in Statistics for more than 2 years now.I am a subject expert in Statistics with Assignmentpedia.com.

3+ Reviews

10+ Question Solved

Related Book For

Corporate Finance Core Principles and Applications

ISBN: 978-1259289903

5th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

Question Posted: