This morning you agreed to buy a 1-year Treasury bond in 6 months. The bond has a

Question:

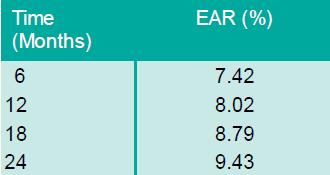

This morning you agreed to buy a 1-year Treasury bond in 6 months. The bond has a face value of £100,000. Use the spot interest rates listed here to answer the following questions:

(a) What is the forward price of this contract?

(b) Suppose shortly after you purchased the forward contract, all rates increased by 30 basis points. For example, the 6-month rate increased from 7.42 per cent to 7.72 per cent. What is the price of a forward contract otherwise identical to yours given these changes?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Therefore the forward price of ...View the full answer

Answered By

Akshay Singla

as a qualified engineering expert i am able to offer you my extensive knowledge with real solutions in regards to planning and practices in this field. i am able to assist you from the beginning of your projects, quizzes, exams, reports, etc. i provide detailed and accurate solutions.

i have solved many difficult problems and their results are extremely good and satisfactory.

i am an expert who can provide assistance in task of all topics from basic level to advance research level. i am working as a part time lecturer at university level in renowned institute. i usually design the coursework in my specified topics. i have an experience of more than 5 years in research.

i have been awarded with the state awards in doing research in the fields of science and technology.

recently i have built the prototype of a plane which is carefully made after analyzing all the laws and principles involved in flying and its function.

1. bachelor of technology in mechanical engineering from indian institute of technology (iit)

2. award of excellence in completing course in autocad, engineering drawing, report writing, etc

48+ Reviews

56+ Question Solved

Related Book For

Corporate Finance

ISBN: 9780077173630

3rd Edition

Authors: David Hillier, Stephen A. Ross, Randolph W. Westerfield, Bradford D. Jordan, Jeffrey F. Jaffe

Question Posted: