For a one-period arbitrage-free binomial model with two nondividend-paying securities, you are given: (i) The following price

Question:

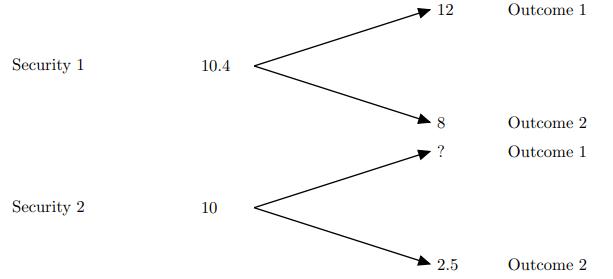

For a one-period arbitrage-free binomial model with two nondividend-paying securities, you are given:

(i) The following price evolution of the two securities:

(ii) The following information about two European call options:

Calculate the current price of call option B.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Call option A pays 12 9 3 in Outcome 1 and 8 9 0 in Outcome 2 To determin...View the full answer

Answered By

Anjali Arora

Having the experience of 16 years in providing the best solutions with a proven track record of technical contribution and appreciated for leadership in enhancing team productivity, deliverable quality, and customer satisfaction. Expertise in providing the solution in Computer Science, Management, Accounting, English, Statistics, and Maths.

Also, do website designing and Programming.

Having 7 yrs of Project Management experience.

100% satisfactory answers.

3+ Reviews

10+ Question Solved

Related Book For

Question Posted: