Suppose the current time is 0. Consider two European put options on the same underlying stock and

Question:

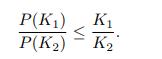

Suppose the current time is 0. Consider two European put options on the same underlying stock and the same maturity date T, but with different strike prices K1 and K2, where K1 ≤ K2. The prices of the above options are denoted by P(K1) and P(K2), respectively.

Use no-arbitrage arguments to show that

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Certainly The principle of noarbitrage in options pricing suggests that there shouldnt exist an oppo...View the full answer

Answered By

Vincent Omondi

I am an extremely self-motivated person who firmly believes in his abilities. With high sensitivity to task and operating parameters, deadlines and keen on instructions, I deliver the best quality work for my clients. I handle tasks ranging from assignments to projects.

109+ Reviews

314+ Question Solved

Related Book For

Question Posted: