You are given: C(K, T) denotes the current price of a K-strike T-year European call option

Question:

You are given:

• C(K, T) denotes the current price of a K-strike T-year European call option on a nondividend-paying stock.

• P(K, T) denotes the current price of a K-strike T-year European put option on the same stock.

• S denotes the current price of the stock.

• The continuously compounded risk-free interest rate is r.

Which of the following is (are) correct?

(A) (I) only

(B) (II) only

(C) (III) only

(D) (I) and (II) only

(E) (I) and (III) only

Transcribed Image Text:

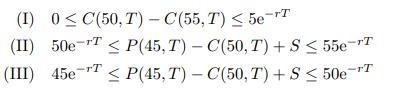

(I) 0 ≤ C(50, T) - C(55, T) ≤ 5e-T

(II) 50e-T

(I) 0 ≤ C(50, T) - C(55, T) ≤ 5e-T

(II) 50e-T

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

E I is true Call price is a decreasing function of K so C50 ...View the full answer

Answered By

Answered By

Dinesh F

I have over 3 years of professional experience as an assignment tutor, and 1 year as a tutor trainee.

1+ Reviews

10+ Question Solved

Dinesh F

I have over 3 years of professional experience as an assignment tutor, and 1 year as a tutor trainee.

1+ Reviews

10+ Question Solved

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

E I is true Call price is a decreasing function of K so C50 ...View the full answer

Answered By

Dinesh F

I have over 3 years of professional experience as an assignment tutor, and 1 year as a tutor trainee.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: