You are given the following information about a securities market: There are two nondividend-paying stocks, X

Question:

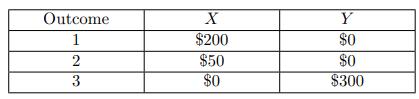

You are given the following information about a securities market:

• There are two nondividend-paying stocks, X and Y .

• The current prices for X and Y are both $100.

• The continuously compounded risk-free interest rate is 10%.

• There are three possible outcomes for the prices of X and Y one year from now:

Let CX be the price of a European call option on X, and PY be the price of a European put option on Y . Both options expire in one year and have a strike price of $95.

Calculate PY − CX.

(A) $4.30

(B) $4.45

(C) $4.59

(D) $4.75

(E) $4.94

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

A Instead of calculating P Y and C X separately we view reg...View the full answer

Answered By

ALUKA ANIL KUMAR

2 years experience in tutoring and mentoring individuals across several subjects.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: