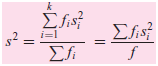

Bartletts homogeneity-of-variance test.* Suppose there are k independent sample variances s 2 1 , s 2 2

Question:

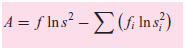

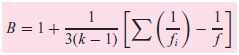

provides an estimate of the common (pooled) estimate of the population variance σ2, where fi = (ni ˆ’ 1), ni being the number of observations in the ith group and where f Σki = 1 fi . Bartlett has shown that the null hypothesis can be tested by the ratio A/B, which is approximately distributed as the χ2 distribution with k ˆ’ 1 df, where

And

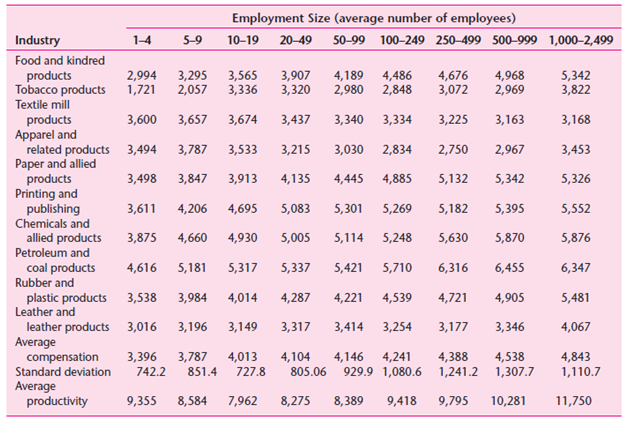

Apply Bartlett€™s test to the data of the following table and verify that the hypothesis that population variances of employee compensation are the same in each employment size of the establishment cannot be rejected at the 5 percent level of significance. Note: fi, the df for each sample variance, is 9, since ni for each sample (i.e., employment class) is 10.

The word "distribution" has several meanings in the financial world, most of them pertaining to the payment of assets from a fund, account, or individual security to an investor or beneficiary. Retirement account distributions are among the most...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Using Bartletts test the ...View the full answer

Answered By

Utsab mitra

I have the expertise to deliver these subjects to college and higher-level students. The services would involve only solving assignments, homework help, and others.

I have experience in delivering these subjects for the last 6 years on a freelancing basis in different companies around the globe. I am CMA certified and CGMA UK. I have professional experience of 18 years in the industry involved in the manufacturing company and IT implementation experience of over 12 years.

I have delivered this help to students effortlessly, which is essential to give the students a good grade in their studies.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: