Consider the following model: R t = β 0 + β 1 M t + β 2

Question:

Rt = β0 + β1Mt + β2Yt + u1t

Yt = α0 + α1Rt + u2t

where Mt (money supply) is exogenous, Rt is the interest rate, and Yt is GDP.

a. How would you justify the model?

b. Are the equations identified?

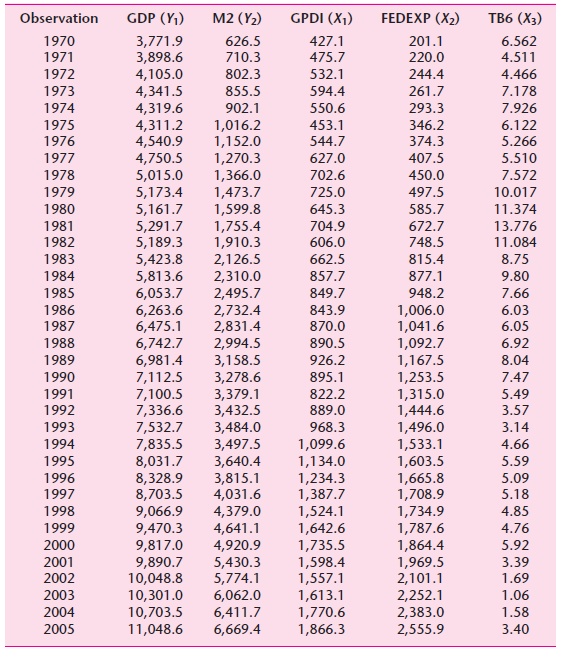

c. Using the data given in the following table, estimate the parameters of the identified equations. Justify the method(s) you use.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a The ISLM model of macroeconomics may be used to justify this model b By the order condi...View the full answer

Answered By

Ashish Jaiswal

I have completed B.Sc in mathematics and Master in Computer Science.

20+ Reviews

39+ Question Solved

Related Book For

Question Posted: