Allow two-party competition in the elections over infinite time horizon, (t=0,1, ldots,+infty). Assume that there is an

Question:

Allow two-party competition in the elections over infinite time horizon, \(t=0,1, \ldots,+\infty\). Assume that there is an election every other period and two parties, \(i=L, R\) ("left" and "right"), compete in the election period to get into power.

Assume that in each period \(t\) the party in power has the opportunity to conduct a credit policy, providing an extra credit supply of \(L_{t}\) to the economy through banks, and assume that an extra \(1 \%\) increase in credit supply \(L_{t}\) leads to \(1 \%\) increase in GDP, \(Y_{t}\). We use lower case alphabets to denote logarithm forms of \(L_{t}\) and \(Y_{t}\), i.e.,

\[l_{t}=\ln L_{t} \text {, and } y_{t}=\ln Y_{t} \text {. }\]

In each period \(t\), voters have an expectation on total output, or, GDP, denoted by \(y_{\tau}^{e}\). With realized GDP \(y_{\tau}\), the surprise to the voters is denoted by

\[\delta_{t}=y_{t}-y_{t}^{e}=l_{t}-l_{t}^{e} .\]

Voters are more likely to vote for the ruling party, if they are positively surprised. On the other hand, a convex political cost is incurred for the credit policy, denoted by a cost function \(c\left(l_{t}\right)\)

\[c\left(l_{t}\right)=\frac{\theta}{2} l_{t}^{2}\]

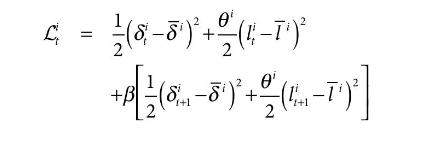

with \(\theta\) being a constant and \(\theta>0\). To balance the gain and the cost, a ruling party \(i\) has targets on \(\delta\) and \(l\), call them \(\bar{\delta}^{i}\) and \(\bar{l}^{i}\), and the loss function for a ruling party in an election cycle is given by

with \(\theta^{i}\) being a constant for party \(i\) and \(\theta^{i}>0, \beta\) being a constant discount factor and \(0& \bar{\delta}^{L} \geq \bar{\delta}^{R} \\

with \(\theta^{i}\) being a constant for party \(i\) and \(\theta^{i}>0, \beta\) being a constant discount factor and \(0& \bar{\delta}^{L} \geq \bar{\delta}^{R} \\

& \bar{l}^{L} \geq \bar{l}^{R} \\

& \theta^{L} \leq \theta^{R} .

\end{aligned}\]

We further assume that voters are rational such that \[l_{t}^{e}=E_{t-1}\left[l_{t}\right] .\]

(a) Compute the optimal choice on \(l_{t}\) for each party, i.e., \(l_{t}^{L}\) and \(l_{t}^{R}\), respectively.

(b) Assume that the probability that party \(L\) wins in period \(t\) is exogenously given as \(p^{L}\). Then before the election, voters' expectation on credit supply can be also expressed as \[l_{t}^{e}=p^{L} l_{t}^{L}+\left(1-p^{L}\right) l_{t}^{R}\]

Compute \(l_{t}^{L}\) and \(l_{t}^{R}\) as functions of \(p^{L}\).

(c) What is the difference in economic performance, between party \(L\) 's and party \(R\) 's first period in power? Does the difference persist in their second period?

Step by Step Answer: