Omega Corporation, a regular C corporation, presents you with the following partial book income statement for the

Question:

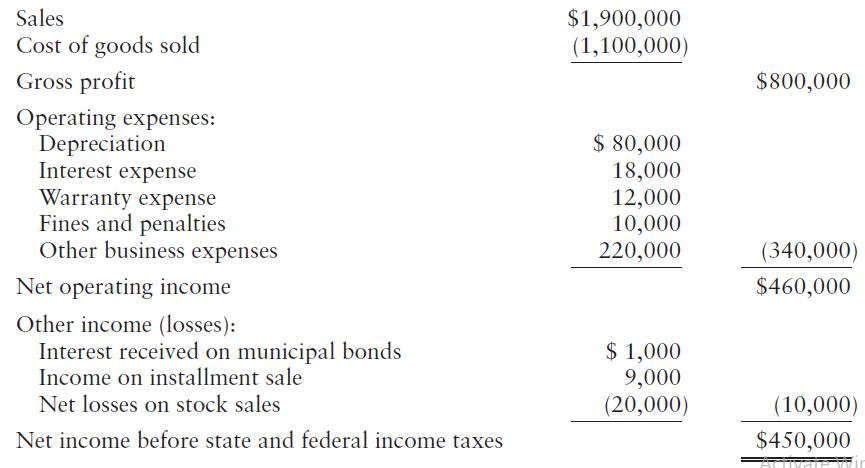

Omega Corporation, a regular C corporation, presents you with the following partial book income statement for the current year:

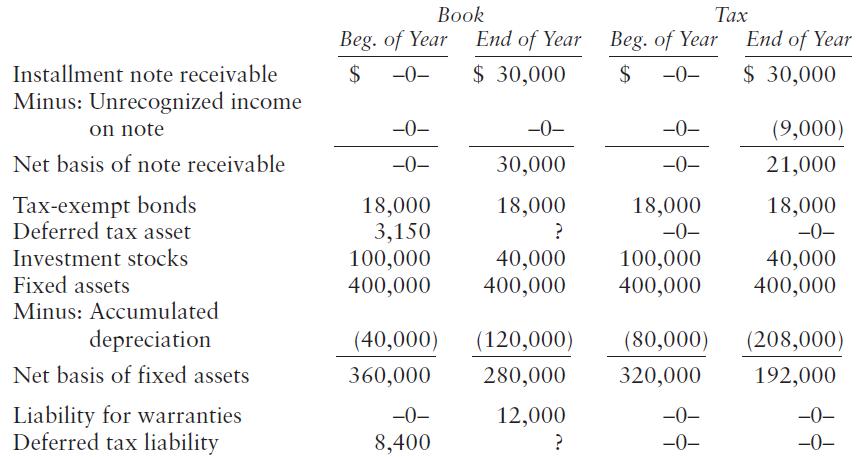

Omega also provides the following partial balance sheet information:

You have gathered the following additional information:

1. Depreciation for tax purposes is $128,000.

2. Of the $18,000 interest expense, $2,000 is allocable to a loan used to purchase the municipal bonds.

3. The warranty expense is an estimated amount for book purposes. Omega expects actual claims on these warranties to be filed and paid next year.

4. Your research determines that the fines and penalties are not deductible for tax purposes.

5. In the current year, Omega sold property using the installment method as follows:

Selling price . . . . . . . . . . . . . . . . . . $30,000

Adjusted basis . . . . . . . . . . . . . . . . . . (21,000)

Gain . . . . . . . . . . . . . . . . . . $9,000

Omega obtains a $30,000 installment note receivable this year and will receive the $30,000 sales proceeds next year. For book purposes, Omega recognizes the $9,000 gain in the current year. For tax purposes, Omega will recognize the $9,000 gain next year when it receives the $30,000 sales proceeds.

6. Omega sold a significant portion of its stock portfolio in the current year. The $20,000 net loss per books from these stock sales includes the following components:

Long-term capital gain . . . . . . . . . . . . . . . . . . $15,000

Long-term capital loss . . . . . . . . . . . . . . . . . . (38,000)

Short-term capital gain . . . . . . . . . . . . . . . . . . 3,000

Omega had no capital gains in prior years, so it cannot carry the net capital losses back.

7. Omega does not expect to realize capital gains next year, but it does expect sufficient capital gains within the next five years so that it can use the capital loss carryover before it expires. Thus, Omega determines that it needs no valuation allowance.

8. Omega has a $15,000 net operating loss carryover from last year, which it then expected to use in the next year (now the current year).

9. Omega incurred and paid $27,000 of state income taxes for the year.

10. Omega’s tax rate is 21% and will remain so in future years.

11. The beginning deferred tax asset pertains to the NOL carryover, and the beginning deferred tax liability pertains to fixed assets. Other deferred tax assets and deferred tax liabilities may arise in the current year.

12. Omega determines that it needs no adjustment for uncertain tax positions.

Required:

Perform the tax provision process steps as outlined in the text. For Step 11, just present partial income statement and balance sheet disclosures as allowed by the given facts.

Step by Step Answer:

Step 1 Identify temporary differences Steps 2 3 Prepare roll forward schedules and apply tax rates Steps 4 5 No valuation allowance or uncertain tax position adjustment needed Step 6 Federal income ta...View the full answer

Federal Taxation 2021 Corporations, Partnerships, Estates & Trusts

ISBN: 9780135919460

34th Edition

Authors: Timothy J. Rupert, Kenneth E. Anderson, David S. Hulse