As we know, there is a requirement within the Corporations Act that financial statements be true and

Question:

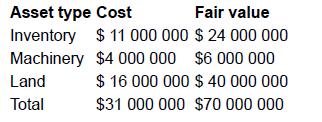

As we know, there is a requirement within the Corporations Act that financial statements be ‘true and fair’. There is also a requirement that company directors comply with accounting standards. In respect of one such standard, AASB 102 Inventories, there is a requirement that inventory be valued at the lower of cost and net realisable value. There is also another accounting standard, AASB 116 Property, Plant and Equipment, which permits property, plant and equipment to be measured at either cost or fair value. Now assume that Angourie Ltd has assets with the following costs and fair values (fair values can be thought of as the amounts that the company expects the assets could be sold for in the normal course of business, and in a transaction between knowledgeable parties that are not related):

In accordance with the options available in the accounting standards, Angourie Ltd decides to measure the assets at cost and therefore discloses the assets in the statement of financial position (balance sheet) at an amount of $31 million, despite the fact that it could receive $70 million for them at that point if it sold them.

Although there is compliance with accounting standards, would such financial statements be ‘true and fair’ if the assets were disclosed at a total of $31 million when they could actually be sold for $70 million?

Step by Step Answer:

The financial statements would be considered to be true and fair if the assets were disclosed at a t...View the full answer