Here?s an advanced version of exercise 10. Consider an alternative parameterization of the binomial: Construct binomial European

Question:

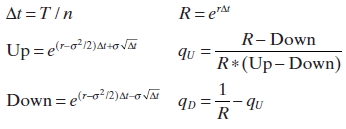

Here?s an advanced version of exercise 10. Consider an alternative parameterization of the binomial:

Construct binomial European call and put option pricing functions in VBA for this parameterization and show that they also converge to the Black-Scholes formula.?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Option Explicit Function BinomialEuropeanCallS As Double K As Double T As Double r As Double sigma As Double n As Integer As Double Dim dt As Double D...View the full answer

Answered By

Aketch Cindy Sunday

I am a certified tutor with over two years of experience tutoring . I have a passion for helping students learn and grow, and I firmly believe that every student has the potential to be successful. I have a wide range of experience working with students of all ages and abilities, and I am confident that I can help students succeed in school.

I have experience working with students who have a wide range of abilities. I have also worked with gifted and talented students, and I am familiar with a variety of enrichment and acceleration strategies.

I am a patient and supportive tutor who is dedicated to helping my students reach their full potential. Thank you for your time and consideration.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: