In November 2008 the Belgian InBev S.A. completed the acquisition of US-based Anheuser-Busch. The brewer acquired Anheuser-Busch

Question:

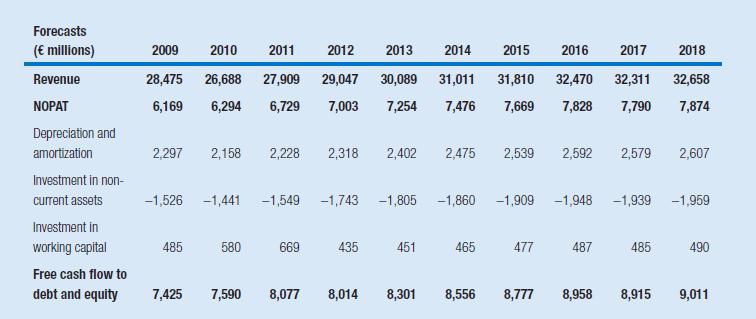

In November 2008 the Belgian InBev S.A. completed the acquisition of US-based Anheuser-Busch. The brewer acquired Anheuser-Busch for close to €40 billion, of which it classified approximately €25 billion as goodwill. At the end of the fiscal year ending on December 31, 2008, Anheuser-Busch InBev’s (AB InBev) net assets amounted to €61,357 million, consisting of €64,183 million in non-current assets and−€2,826 million in working capital. The company’s book value of equity amounted to €16,126 million.

Early May, 2009, when AB Inbev’s 1,593 million common shares trade at about €24 per share, an analyst produces the following forecasts for the company and issues an “overweight” (buy) recommendation.

1 The analyst estimates that AB InBev’s weighted average cost of capital is 9 percent and assumes that the free cash flow to debt and equity grows

indefinitely at a rate of 1 percent after 2018. Show that under these assumptions the equity value per share estimate exceeds AB InBev’s share price.

2 Calculate AB InBev’s expected abnormal NOPATs between 2009 and 2018 based on the preceding information. How does the implied trend in abnormal NOPAT compare with the general trends in the economy?

3 Estimate AB InBev’s equity value using the abnormal NOPAT model (under the assumption that the WACC is 9 percent and the terminal growth rate is 1 percent). Why do the discounted cash flow model and the abnormal NOPAT model yield different outcomes?

4 What adjustments to the forecasts are needed to make the two valuation models consistent?

Step by Step Answer:

Business Analysis And Valuation

ISBN: 978-1473758421

5th Edition

Authors: Erik Peek, Paul Healy, Krishna Palepu