Question:

The cigarette industry is subject to litigation for health hazards posed by its products. In the United States, the industry has been negotiating a settlement of these claims with state and federal governments.

As the CFO for UK-based British American Tobacco (BAT), which is affected through its US subsidiaries, what information would you report to investors in the annual report on the firm’s litigation risks? How would you assess whether the firm should record a provision for this risk, and if so, how would you assess the value of this provision? As a financial analyst following BAT, what questions would you raise with the CFO over the firm’s litigation provision?

British American Tobacco example

Transcribed Image Text:

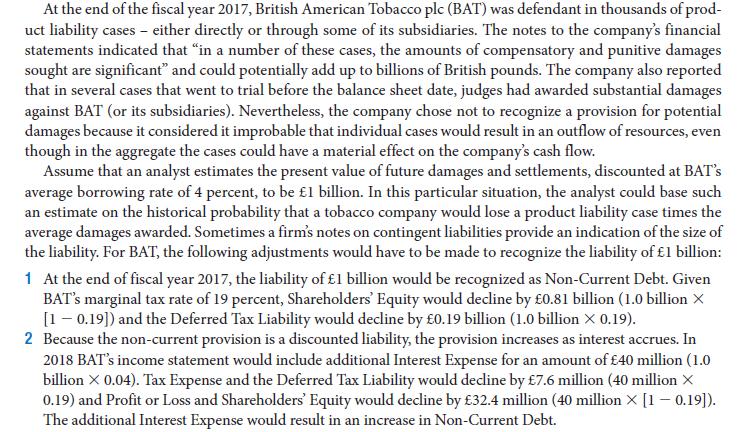

At the end of the fiscal year 2017, British American Tobacco plc (BAT) was defendant in thousands of prod- uct liability cases - either directly or through some of its subsidiaries. The notes to the company's financial statements indicated that "in a number of these cases, the amounts of compensatory and punitive damages sought are significant" and could potentially add up to billions of British pounds. The company also reported that in several cases that went to trial before the balance sheet date, judges had awarded substantial damages against BAT (or its subsidiaries). Nevertheless, the company chose not to recognize a provision for potential damages because it considered it improbable that individual cases would result in an outflow of resources, even though in the aggregate the cases could have a material effect on the company's cash flow. Assume that an analyst estimates the present value of future damages and settlements, discounted at BAT's average borrowing rate of 4 percent, to be 1 billion. In this particular situation, the analyst could base such an estimate on the historical probability that a tobacco company would lose a product liability case times the average damages awarded. Sometimes a firm's notes on contingent liabilities provide an indication of the size of the liability. For BAT, the following adjustments would have to be made to recognize the liability of 1 billion: 1 At the end of fiscal year 2017, the liability of 1 billion would be recognized as Non-Current Debt. Given BAT's marginal tax rate of 19 percent, Shareholders' Equity would decline by 0.81 billion (1.0 billion X [10.19]) and the Deferred Tax Liability would decline by 0.19 billion (1.0 billion X 0.19). 2 Because the non-current provision is a discounted liability, the provision increases as interest accrues. In 2018 BAT's income statement would include additional Interest Expense for an amount of 40 million (1.0 billion X 0.04). Tax Expense and the Deferred Tax Liability would decline by 7.6 million (40 million X 0.19) and Profit or Loss and Shareholders' Equity would decline by 32.4 million (40 million X [1-0.19]). The additional Interest Expense would result in an increase in Non-Current Debt.