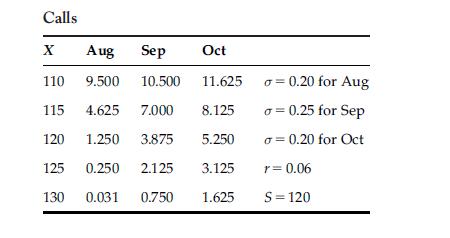

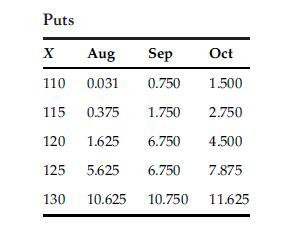

Evaluate each of the European options in the series on ABC Company stock. Prices for each of

Question:

Evaluate each of the European options in the series on ABC Company stock. Prices for each of the options are listed in the table. Determine whether each of the options in the series should be purchased or sold at the given market prices. The current market price of ABC stock is 120, the August options expire in nine days, September options in 44 days, and October options in 71 days. The stock return standard deviations prior to expirations are projected to be 0.20 prior to August, 0.25 prior to September, and 0.20 prior to October.

The Treasury bill rate is projected to be 0.06 for each of the three periods prior to expiration. Do not forget to convert the number of days given to fractions of 365-day years.

Prices for five calls and five puts are given in the left columns. Expiration dates are given in column headings and current market prices are given in the table interiors.

Step by Step Answer:

Value the calls using the BlackScholes model c 0 S 0 Nd 1 Xe rT Nd 2 d 1 ln S X r 05 2 ...View the full answer