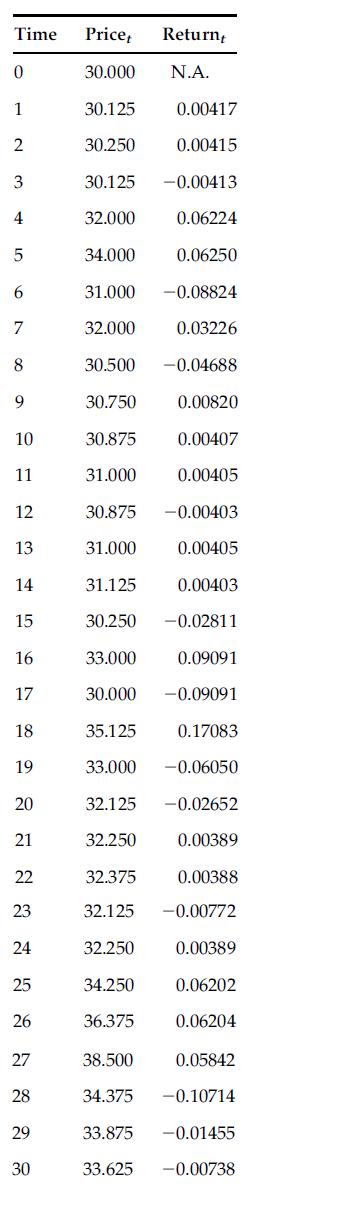

The following table presents sample daily historical price data for a stock whose returns are given in

Question:

The following table presents sample daily historical price data for a stock whose returns are given in the third column.

a. Based on a traditional sample estimator, calculate a daily variance estimator for this stock.

b. Assume that returns follow a Brownian motion process (at least that stock returns are uncorrelated over time) and that there are 30 trading days per month. What would be the monthly variance for this stock?

c. What would be the Parkinson extreme value estimated daily returns variance for this stock?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a The daily population variance is 0003066 The daily sample ...View the full answer

Answered By

Joram mutua

I am that writer who gives his best for my student/client. Anything i do, i give my best. I have tutored for the last five years and non of my student has ever failed, they all come back thanking me for the best grades. I have a degree in economics, but i have written academic papers for various disciplines due to top-notch research Skills.In additional, I am a professional copywriter and proofreader.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: