The following table reflects abnormal returns for each of 10 stocks over a seven-day period about day

Question:

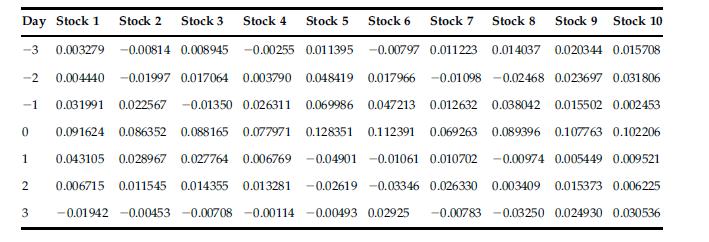

The following table reflects abnormal returns for each of 10 stocks over a seven-day period about day zero, which is the standardized date of the sudden death of the CEO for each of the 10 firms. An analyst wants to determine whether the death announcement date represents a significant event and make appropriate portfolio adjustments when CEOs suddenly die in the future.

a. What are the average residuals, their standard deviations, and normal deviates for each of the seven dates?

b. What are the cumulative average residuals, their standard deviations, and normal deviates for each of the seven dates?

c. On which days are average residuals statistically significant at the 1% level? On which days are cumulative average residuals statistically significant at the 1%

level?

Step by Step Answer:

a Average residuals standard deviations and normal deviates are give...View the full answer