A fixed-income analyst is considering the credit risk over the next year for three corporate bonds currently

Question:

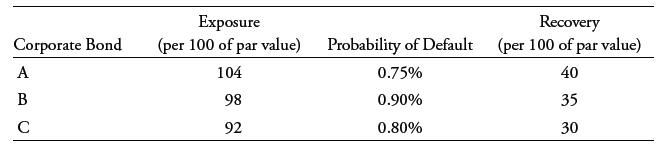

A fixed-income analyst is considering the credit risk over the next year for three corporate bonds currently held in her bond portfolio. Her assessment for the exposure, probability of default, and recovery is summarized in this table:

Although all three bonds have very similar yields to maturity, the differences in the exposures arise because of differences in their coupon rates. Based on these assumptions, how would she rank the three bonds, from highest to lowest, in terms of credit risk over the next year?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

She needs to get the loss given default for each bo...View the full answer

Answered By

Wahome Michael

I am a CPA finalist and a graduate in Bachelor of commerce. I am a full time writer with 4 years experience in academic writing (essays, Thesis, dissertation and research). I am also a full time writer which assures you of my quality, deep knowledge of your task requirement and timeliness. Assign me your task and you shall have the best.

Thanks in advance

63+ Reviews

132+ Question Solved

Related Book For

Question Posted: