A portfolio manager considers the following annual coupon bonds: An increase in expected inflation causes the government

Question:

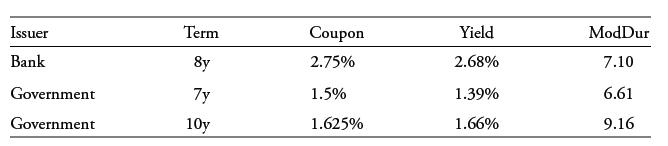

A portfolio manager considers the following annual coupon bonds: An increase in expected inflation causes the government yield curve to steepen, with a 20-point rise in the 10-year government bond YTM and no change in the 7-year government YTM. If the respective bank bond yield spread measures remain unchanged, calculate the expected bank bond percentage price change in each case, and explain which is a more accurate representation of the market change in this case.

An increase in expected inflation causes the government yield curve to steepen, with a 20-point rise in the 10-year government bond YTM and no change in the 7-year government YTM. If the respective bank bond yield spread measures remain unchanged, calculate the expected bank bond percentage price change in each case, and explain which is a more accurate representation of the market change in this case.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

For the yield spread measure neither the 120 spread nor the 7year government rate of 139 has changed ...View the full answer

Answered By

Jehal Shah

I believe everyone should try to be strong at logic and have good reading habit. Because If you possess these two skills, no matter what difficult situation is, you will definitely find a perfect solution out of it. While logical ability gives you to understand complex problems and concepts quite easily, reading habit gives you an open mind and holistic approach to see much bigger picture.

So guys, I always try to explain any concept keeping these two points in my mind. So that you will never forget any more importantly get bored.

Last but not the least, I am finance enthusiast. Big fan of Warren buffet for long term focus investing approach. On the same side derivatives is the segment I possess expertise.

If you have any finacne related doubt, do reach me out.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: