The factor that is currently least likely to affect the riskreturn characteristics of Bond #9 is: A.

Question:

The factor that is currently least likely to affect the risk–return characteristics of Bond #9 is:

A. Interest rate movements.

B. Whorton’s credit spreads.

C. Whorton’s common stock price movements.

Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond portfolio. Rayes has asked Mingfang Hsu, one of the firm’s analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm’s bond portfolio.

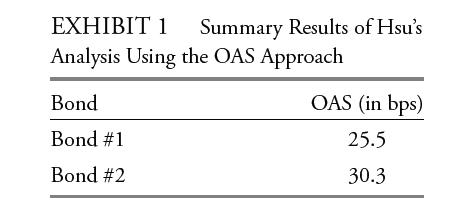

Hsu first selects two corporate bonds that are callable at par and have the same characteristics in terms of maturity, credit quality, and call dates. Hsu uses the option adjusted spread (OAS) approach to analyze the bonds, assuming an interest rate volatility of 10%. The results of his analysis are presented in Exhibit 1.

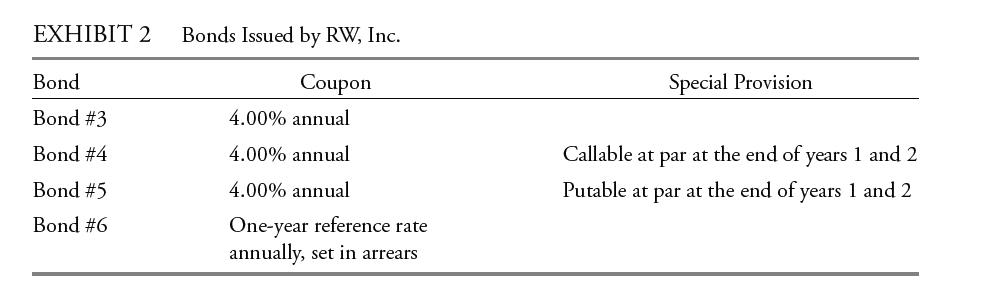

Hsu then selects the four bonds issued by RW, Inc., given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds #4 and #5 are identical to Bond #3, an option-free bond, except that they each include an embedded option.

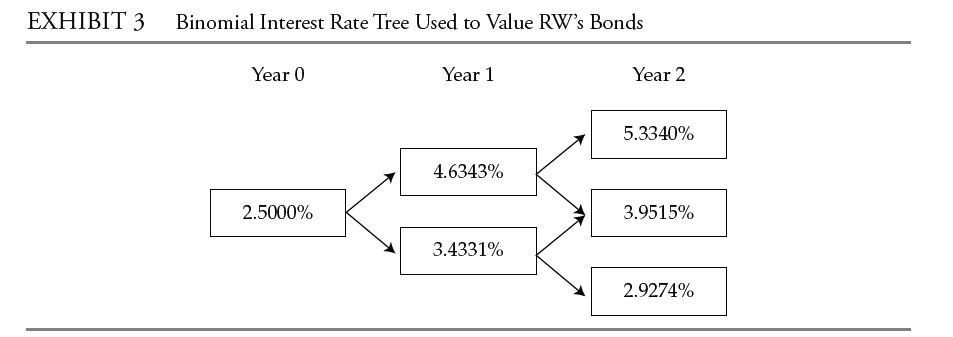

To value and analyze RW’s bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond #4’s price to a 20 bps parallel shift of the benchmark yield curve. The results of Hsu’s calculations are shown in Exhibit 4.

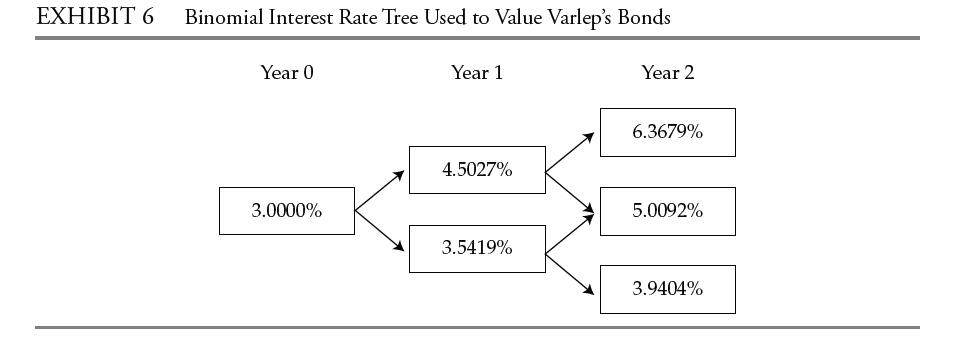

Hsu also selects the two floating-rate bonds issued by Varlep, plc, given in Exhibit 5. These bonds have a maturity of three years and the same credit rating.

To value Varlep’s bonds, Hsu constructs the binomial interest rate tree provided in Exhibit 6.

Last, Hsu selects the two bonds issued by Whorton, Inc., given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond #9 includes a conversion option. Whorton’s common stock is currently trading at $30 per share.

Step by Step Answer: