The Phillips Toy Company was considering the advisability of adding a new product line. Ike Barnes, a

Question:

By late 2015, however, the need to generate additional new product lines was becoming evident, as sales had been flat for the past three years and expected 2015 profit actually looked as if it might be 5 percent or so less than 2014's $2 million. After doing a market analysis of possible product additions, Barnes decided that the hockey card market was a booming area for potential new and profitable sales. Hockey cards were popular not only among youngsters, but also among adults trying to recapture some of their youthful experiences.

Although his marketing surveys had indicated this to be a strong growth market, albeit with substantial competition, Barnes had to compile a thorough capital budgeting analysis for consideration by the executive committee of the company. In the previous new product projects with which he had been involved, his predecessor, John Smith, had done all of the financial analysis, and Barnes wished now that he had paid more attention to that part of the process. He remembered he had not been partie ularly good in finance as a student.

In evaluating the market potential, Barnes determined that there was no way he could predict the market penetration potential for a new set of hockey cards. The sales for the set, which would be called Hockey Legends, would depend on the quality of the final product as well as the effectiveness of the promotional activities. There was also the danger of errors when the set was initially issued. With approximately 400 cards in the set, there could be incorrect scoring statistics, ages, and so forth. When Johnson & Smith introduced its new set in 2004, the cards were highly criticized by collectors because of numerous factual errors. Barnes hoped to avoid this problem for the Hockey Legends set. He intended to hire people experienced in the sports card or publishing business to identify potential problems at an early stage.

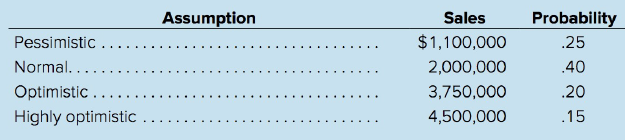

Ike Barnes knew that, over the years, Phillips had developed a manual for evaluating capital budgeting projects. As a first step, in conjunction with the sales manager, Barnes predicted anticipated sales over the next six years. Although he thought this too short a time period to evaluate the full potential of the project, he had no choice but to go along with company policy. He decided to start by projecting a wide range for potential sales in 2016, the first year in which there would be sales. He then assigned probabilities to the outcomes as shown in Table 1.

Barnes's intention was to determine the expected value for sales for the first year and then project a 20 percent growth rate for the next three years, and 10 percent for the final two years of the forecast period. Operating expenses were expected to average approximately 70 percent of sales. The primary investment to be made was in printing and production equipment, which would fall into Class 8 for CCA purposes. The equipment was forecast to cost $2.8 million and represented virtually the total capital investment for the business, except for about $200,000 in working capital.

Barnes looked into the capital budgeting manual to determine the appropriate discount rate, as he had seen a number of different ones used throughout the company. The manual stated that the discount rate was to be based on the coefficient of variation of the first year's sales projections, based on the categories shown in Table 2. Barnes was a little concerned that these categories and rates had been struck a few years earlier when interest rates were generally a couple of percentage points higher, and he wondered if that should make any difference.

Ike Barnes knew top management was eager for him to present a business plan that would be approved and implemented soon. Thus, he was interested in calling his assistants together to get the analysis done immediately so it could be presented, along with a recommendation, at the next meeting of the executive committee.

Table 1

Table 2

Coefficient of variation .............................Appropriate discount rate

0-.20 ...................................................................8%

.2 1-.40 .............................................................10

.4 1- .60.............................................................14

.61 - .80.............................................................16

Over .80.............................................................20

Capital budgeting is a practice or method of analyzing investment decisions in capital expenditure, which is incurred at a point of time but benefits are yielded in future usually after one year or more, and incurred to obtain or improve the... Discount Rate

Depending upon the context, the discount rate has two different definitions and usages. First, the discount rate refers to the interest rate charged to the commercial banks and other financial institutions for the loans they take from the Federal...

Step by Step Answer:

Capital Budgeting and Cash Flow Purpose The case gives the student a good opportunity to do cash flow analysis The use of variable discount rates based on project risk gives insight into how some corp...View the full answer

Foundations of Financial Management

ISBN: 978-1259024979

10th Canadian edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta