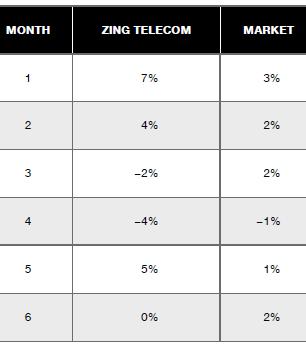

a. Given the holding-period returns shown here, compute the average returns and the standard deviations for Zing

Question:

a. Given the holding-period returns shown here, compute the average returns and the standard deviations for Zing Telecom and for the market.

b. If Zing’s beta is 1.67 and the risk-free rate is 5 percent, what would be an appropriate required return for an investor owning Zing? Because the returns of Zing Telecom are based on monthly data, you will need to annualize the returns to make them compatible with the risk-free rate. For simplicity, you can convert from monthly to yearly returns by multiplying the average monthly returns by 12.

c. How does Zing’s historical average return compare with the return you believe to be appropriate, given the firm’s systematic risk?

Step by Step Answer:

Foundations Of Finance

ISBN: 9781292318738

10th Global Edition

Authors: Arthur Keown, John Martin, J. Petty