Compute Sharpe ratios, Treynor ratios, and Jensens alphas for Portfolios A, B, and C based on the

Question:

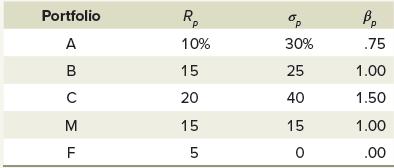

Compute Sharpe ratios, Treynor ratios, and Jensen’s alphas for Portfolios A, B, and C based on the following returns data, where M and F stand for the market portfolio and risk-free rate, respectively:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Using Equations 131 132 and 134 yields the...View the full answer

Answered By

Shehar bano

I have collective experience of more than 7 years in education. my area of specialization includes economics, business, marketing and accounting. During my study period I remained engaged with a business school as a visiting faculty member and did a lot of business research. I am also tutoring and mentoring number of international students and professionals online for the last 7 years.

4+ Reviews

10+ Question Solved

Related Book For

Fundamentals Of Investments Valuation And Management

ISBN: 9781266824012

10th Edition

Authors: Bradford Jordan, Thomas Miller, Steve Dolvin

Question Posted: