Question:

International Reporting Case Walgreens (USA) is the leading drug store chain in the United States. The company provided the following disclosures related to its retirement benefits in its 2013 annual report.

Instructions Use the information on Walgreens to respond to the following requirements.

(a) What are the key differences in accounting for pensions under U.S. GAAP and IFRS?

(b) Briefly explain how differences in U.S. GAAP and IFRS for pensions would affect the amounts reported in the financial statements.

(c) In light of the differences identified in (b), would Walgreens’ income and equity be higher or lower under U.S. GAAP compared to IFRS standards? Explain.

Transcribed Image Text:

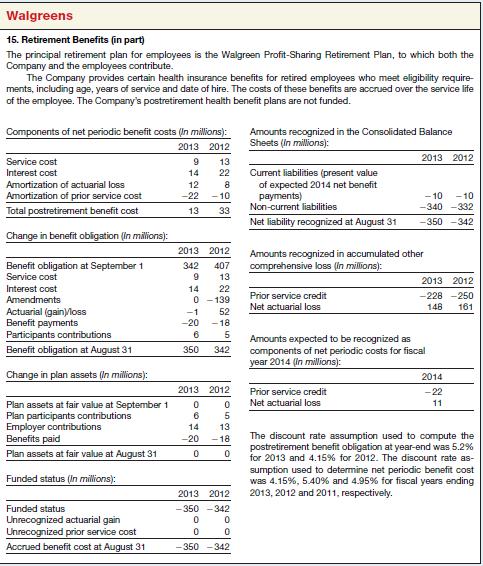

Walgreens 15. Retirement Benefits (in part) The principal retirement plan for employees is the Walgreen Profit-Sharing Retirement Plan, to which both the Company and the employees contribute. The Company provides certain health insurance benefits for retired employees who meet eligibility require- ments, including age, years of service and date of hire. The costs of these benefits are accrued over the service life of the employee. The Company's postretirement health benefit plans are not funded. Components of net periodic benefit costs (in millions): 2013 2012 Amounts recognized in the Consolidated Balance Sheets (in millions): 2013 2012 Service cost 9 13 Interest cost 14 22 Current liabilities (present value Amortization of actuarial loss 12 8 Amortization of prior service cost -22 -10 of expected 2014 net benefit payments) Total postretirement benefit cost 13 33 Non-current liabilities -10 -340-332 -10 Net liability recognized at August 31 -350 -342 Change in benefit obligation (in millions): 2013 2012 Benefit obligation at September 1 342 407 Amounts recognized in accumulated other comprehensive loss (in millions): Service cost 9 13 2013 2012 Interest cost 14 22 Amendments 0-139 Prior service credit Net actuarial loss -228-250 148 161 Actuarial (gain)/loss -1 52 Benefit payments -20 -18 Participants contributions 6 5 Benefit obligation at August 31 350 342 Amounts expected to be recognized as components of net periodic costs for fiscal year 2014 (in millions): Change in plan assets (In millions): Plan assets at fair value at September 1 2013 2012 Prior service credit 0 0 Net actuarial loss 2014 -22 11 Plan participants contributions 6 5 Employer contributions 14 13 Benefits paid -20 -18 Plan assets at fair value at August 31 0 0 Funded status (in millions): Funded status Unrecognized actuarial gain Unrecognized prior service cost Accrued benefit cost at August 31 2013 2012 -350-342 0 0 0 0 -350-342 The discount rate assumption used to compute the postretirement benefit obligation at year-end was 5.2% for 2013 and 4.15% for 2012. The discount rate as- sumption used to determine net periodic benefit cost was 4.15%, 5.40% and 4.95% for fiscal years ending 2013, 2012 and 2011, respectively.