The following three situations involve the capitalization of interest. Situation I: On January 1, 2025, Ohno, Inc.

Question:

The following three situations involve the capitalization of interest.

Situation I: On January 1, 2025, Ohno, Inc. signed a fixed-price contract to have Builder Associates construct a major plant facility at a cost of $4,000,000. It was estimated that it would take 3 years to complete the project. Also on January 1, 2025, to finance the construction cost, Ohno borrowed $4,000,000 payable in 10 annual installments of $400,000, plus interest at the rate of 10%. During 2025, Ohno made deposit and progress payments totaling $1,500,000 under the contract; the weighted-average amount of accumulated expenditures was $800,000 for the year. The excess borrowed funds were invested in short-term securities, from which Ohno realized investment income of $250,000.

Instructions

What amount should Ohno report as capitalized interest at December 31, 2025?

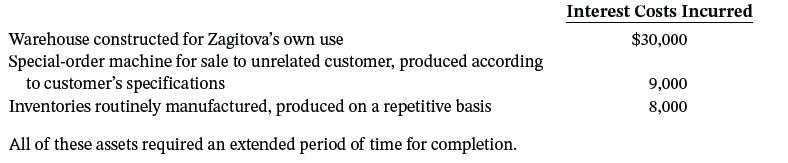

Situation II: During 2025, Zagitova Corporation constructed and manufactured certain assets and incurred the following interest costs in connection with those activities.

Instructions

Assuming the effect of interest capitalization is material, what is the total amount of interest costs to be capitalized?

Situation III: Fleming, Inc. has a fiscal year ending April 30. On May 1, 2025, Fleming borrowed $10,000,000 at 11% to finance construction of its own building. Repayments of the loan are to commence the month following completion of the building. During the year ended April 30, 2026, expenditures for the partially completed structure totaled $7,000,000 (weighted-average accumulated expenditures were $3,500,000). Interest earned on the unexpended portion of the loan amounted to $650,000 for the year.

Instructions

How much should be shown as capitalized interest on Fleming’s financial statements at April 30, 2026?

Step by Step Answer:

Situation I 80000The requirement is the amount Ohno should report as capitalized interest at 123125 The amount of interest eligible for capitalization ...View the full answer

Intermediate Accounting

ISBN: 9781119790976

18th Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield